The Economist - Finance and economics

The French government experiments with venture capitalism

Don’t be coy, carp about the food

{kind=link}

AS A boy, Antoine Hubert used to catch butterflies. These days, the agro-engineer has eyes only for meal worms. In a demonstration factory near Dole in eastern France, he shows how trayfuls of plump, half-grown worms are fed, left to grow in a darkened dormitory, and then—after two months—slaughtered and cleaned with a blast of steam. A machine divides the resulting mush into oil and protein powder.

Around 70% of a worm is protein, making it ideal for animal feed. Demand is soaring, notably at fish and shrimp farms. Mr Hubert predicts aquaculture businesses will need 70m tons of feed annually in ten years’ time, up from 40m now. The global market for animal feed, he reckons, is already worth €500bn ($610bn).

Ynsect, his firm, thus expects to grow once it opens a new factory this year. He dreams of annual output exceeding 1m tonnes, hinting at a hunger for scale often left unsatisfied in a French entrepreneur: local...

The World Bank’s “ease of doing business” report faces tricky questions

{kind=link}

HOW many days does it take to correct a misleading newspaper interview? Four, in the case of Paul Romer, the World Bank’s chief economist. On January 12th a surprising article in the Wall Street Journal alleged that one of the bank’s signature reports—on the ease of doing business around the world—may have been tainted by the political motivations of bank staff. The story was based on an interview with Mr Romer, who pointed out that Chile’s ranking in the yearly report had dropped sharply during the presidency of Michelle Bachelet, a left-leaning politician who took office for the second time in 2014. Chile sank so heavily not because doing business had become harder, but because the bank had repeatedly changed its method of assessment.

That method mostly entails answering measurable questions, such as how many days does it take to start a business, register a property or file taxes. The answers determine a country’s score (known as its “distance to the...

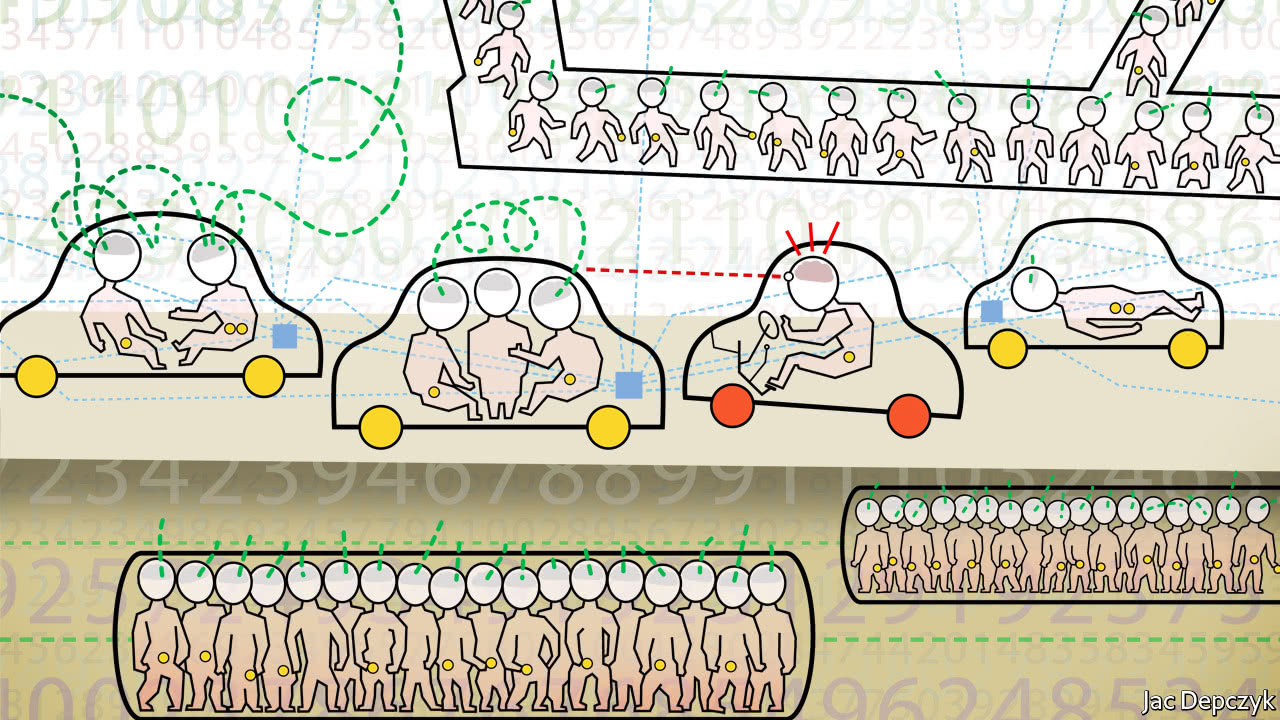

Why driverless cars may mean jams tomorrow

{kind=link}

THE most distractingly unrealistic feature of most science fiction—by some margin—is how the great soaring cities of the future never seem to struggle with traffic. Whatever dystopias lie ahead, futurists seem confident we can sort out congestion. If hope that technology will fix traffic springs eternal, history suggests something different. Transport innovation, from railways to cars, reshaped cities and drove economic advance. But it also brought crowded commutes. Now, as tech firms and carmakers aim to roll out fleets of driverless cars, it is worth asking: might this time be different? Alas, artificial intelligence (AI) is unlikely to succeed where steel rails and internal-combustion engines failed.

More’s the pity. In America alone, traffic congestion brings economic losses estimated in the hundreds of billions of dollars each year. Such costs will rise unless existing transport systems receive badly needed investment. For example, fixing New York’s beleaguered, overcrowded subway will...

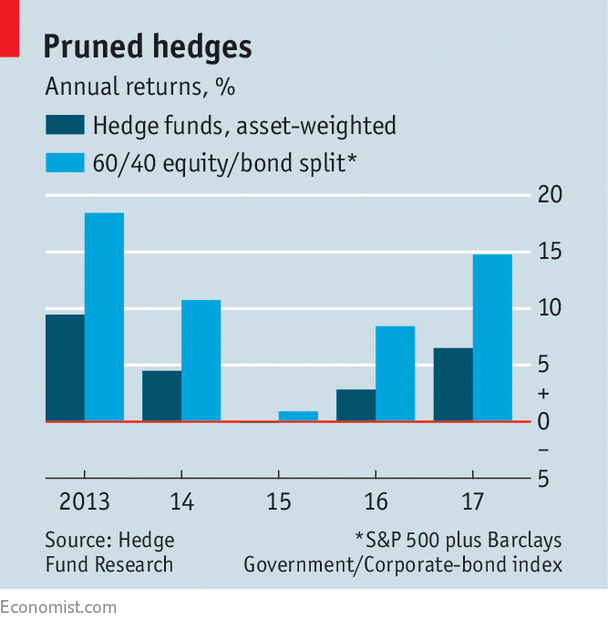

The hedge-fund delusion that grips pension-fund managers

HEDGE-FUND managers may be feeling quietly smug about their performance in 2017. They returned 6.5% on average, according to Hedge Fund Research, a data provider, their best year since 2013.

But those returns do not really suggest that they are masters of the investing universe. The S&P 500 index, America’s main equity benchmark, returned 21.8%, including dividends, last year. More tellingly, a portfolio split 60-40 between the S&P 500 and a mixture of government and corporate bonds (an oft-used benchmark for institutional portfolios) would have returned 14.8%. Last year was the fifth in a row when hedge funds underperformed the 60/40 split (see chart).

{kind=link}

That ought to be a salutary lesson for those institutions who think that backing hedge funds is the answer to their prayers. Despite the highs recorded by stockmarkets, many employers are struggling to fund their final-salary pension promises. In 2016 the average American public-sector plan was just 68%-funded, according to the Centre...

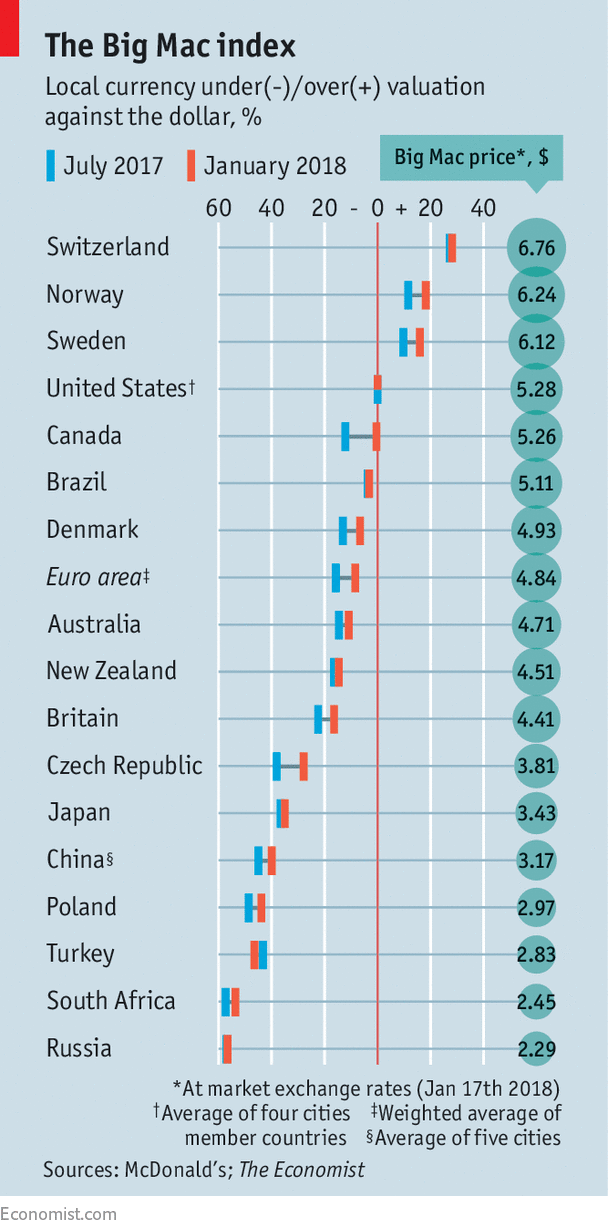

Our Big Mac index shows fundamentals now matter more in currency markets

IT IS usually considered quaint to predict foreign-exchange movements by reference to whether currencies are dear or cheap. Metrics such as The Economist’s Big Mac index, a lighthearted guide to exchange rates, hint at how far currency values are out of whack. But they are often driven further out of kilter by capital flows, by fear and greed, by the interventions of policymakers, and so on.

Since our last look at the index in July, cheap currencies have narrowed the valuation gap against the dollar—almost completely in case of the Canadian dollar (see chart). Fundamentals, such as fair value, seem (at last) to have greater sway in the foreign-exchange market.

{kind=link}

The index is based on the idea of purchasing-power parity, which says exchange rates should move towards the level that would make the price of a basket of goods the same in different countries. Our basket contains only one item, but it is found in around 120 countries: a Big Mac hamburger. If the local...

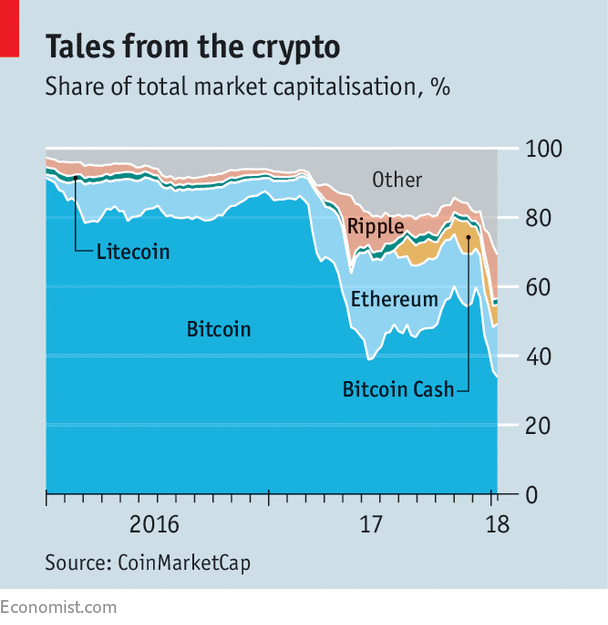

The threat of tough regulation in Asia sends crypto-currencies into a tailspin

{kind=link}

IT HAS been another week of vertiginous swings in the prices of bitcoin and other crypto-currencies. This time, the moves have mostly been downwards, with some days seeing falls of over 20%. Views on this were as divided as they were during the giddy climb: did it mark the definitive bursting of a bubble as rapidly inflated as any in history (see chart)?

{kind=link}

Asia provides both an explanation of this week’s sell-off and a glimpse of crypto-currencies’ future. The threat of a ban in bitcoin-trading in South Korea was the proximate cause of the plunge. As to the future, the question is which Asia? At one end of the...

Why the oil price is so high

{kind=link}

PERHAPS the most vexing thing for those watching the oil industry is not the whipsawing price of a barrel. It is the constant updating of theories to explain what lies behind it. In March 2014, when the price of a barrel of Brent crude was in three figures, the then boss of Chevron, an oil giant, observed that the scarcity of cheap oil meant “$100 per barrel is becoming the new $20”. Two years later, when the oil price slumped below $28, the talk was of a global oil glut caused by the furious efforts of the OPEC cartel to regain market share. Now that oil prices have tested $70, analysts are again scratching their heads.

In “1984”, George Orwell coined the term “doublethink”, the ability to believe two contradictory things. Oil analysis seems to require similar cognitive gymnastics. Three big questions arise. First, why has the oil price more than doubled in the space of two years, against all expectation? Second, why has this surge been met with cheers from global stockmarkets and not...

How China won the battle of the yuan

“THE horse may be out of the proverbial barn.” So wrote Ben Bernanke, a former chairman of the Federal Reserve, in early 2016, arguing that capital controls might be powerless to save China from a run on its currency. He was far from alone at the time. As cash rushed out of the country, analysts debated whether the yuan would collapse, and some hedge funds bet that day was coming fast. But two years on, the horse is back in the barn: the government’s defence of the yuan has succeeded, in part through tighter capital controls.

The latest evidence was an 11th consecutive monthly increase in foreign-exchange reserves in December. During that time China’s stockpile of official reserves, the world’s biggest, climbed by $142bn, reaching $3.14trn, roughly double the cushion usually regarded as needed to ensure financial stability. Another sign of China’s success is the yuan itself. At the start of 2017 the consensus of forecasters was that the currency would continue to weaken; it finished the year up by 6% against the dollar.

Investors and analysts were not wrong in viewing Chinese capital controls as porous. Enterprising types had—and have—umpteen ways to sneak money out, from overpaying for imports to smuggling cash across the border in luggage. But there is a wide spectrum between a fully open and fully closed capital account, and China has showed over...

Accountancy takes root in the inhospitable soil of Afghanistan

{kind=link}

WHEN Afghan lawmakers were debating rules of conduct for accountants, some were confounded by their strictness. Why should those found guilty of murder, asked one member of parliament, be struck off? That is a sign of the challenges facing the professional body for bean-counters, Certified Professional Accountants (CPA) Afghanistan, which was launched last month.

Attempts to establish a home-grown profession start from a low base. Back in 2009 Kabul, a city of around 4m, had fewer than 20 qualified accountants. Neither standards nor oversight for the profession were in place. Most local outfits were branches of firms from elsewhere in South Asia or farther afield.

Boring old accountancy might not seem a priority for a war-torn country. But in business it can foster trust and transparency—scarce commodities in a country where corruption is systemic. Because of the difficulty of verifying borrowers’ financial positions and...

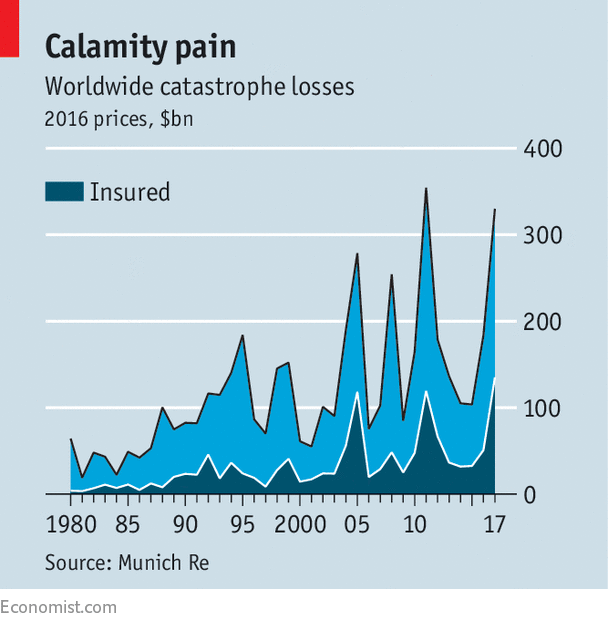

Natural disasters made 2017 a year of record insurance losses

THAT 2017 suffered from more than its fair share of natural catastrophes was known at the time. In the wake of Hurricane Harvey, the streets of Houston, Texas, were submerged under brown floodwater; Hurricane Irma razed buildings to the ground on some Caribbean islands. That the destruction was great enough for insurance losses to reach record levels has only just been confirmed. According to figures released on January 4th by Munich Re, a reinsurer, global, inflation-adjusted insured catastrophe losses reached an all-time high of $135bn in 2017 (see chart). Total losses (including uninsured ones) reached $330bn, second only to losses of $354bn in 2011.

{kind=link}

A large portion of the losses in 2011 was caused by one catastrophe: the earthquake and tsunami in Japan. Losses in 2017 were largely traceable to extreme weather. Fully 97% were weather-related, well above the average since 1980 of 85%. If climate change brings more frequent extreme weather, as Munich Re and others expect, last year’s loss levels...

Donald Trump’s difficult decision on steel imports

{kind=link}

EVERY Tuesday, senior members of the administration gather in the White House to discuss trade. They are divided between hawks, who argue that America needs to be tougher in its defence against what they see as economic warfare waged by China, and doves, who worry about the costs of conflict. So far, against all expectations when President Donald Trump entered the White House, the doves have prevailed. The first of a series of legal deadlines could soon unleash the hawks.

Last April Wilbur Ross, the commerce secretary, initiated a probe into whether steel imports were a threat to America’s national security. His department pointed to a “dramatic” increase in steel imports over the previous year and to the idling of nearly 30% of America’s steel-production capacity, as imports feed a quarter of its consumption. If the report, due by January 15th, finds imports are a threat, Mr Trump, under Section 232 of the Trade Expansion Act of 1962, will have 90 days to respond.

The report’s...

Bitcoin is no longer the only game in crypto-currency town

IT STARTED as a joke. Dogecoin was launched in 2013 as a bitcoin parody, using as its mascot a Japanese shiba inu dog, a popular internet meme. The crypto-currency was never really used, except for tipping online, and one of its founders has called it quits. But recently its price has soared: on January 7th the dollar value of all Dogecoins in circulation reached $2bn, a sign of how crazy crypto-currency markets have become. It is also a reminder that, for all the focus on bitcoin, it is no longer the only game in town. Its market capitalisation now amounts to only about one-third of the crypto-market (see chart).

{kind=link}

A new crypto-currency is born almost daily, often through an “initial coin offering” (ICO), a form of online crowdfunding. CoinMarketCap, a website, lists about 1,400 digital coins or tokens, including PutinCoin, Sexcoin and InsaneCoin (worth $7m). Most are no more than curiosities, but by January 10th, around 40 had a market capitalisation of more than $1bn.

...Should internet firms pay for the data users currently give away?

{kind=link}

YOU have multiple jobs, whether you know it or not. Most begin first thing in the morning, when you pick up your phone and begin generating the data that make up Silicon Valley’s most important resource. That, at least, is how we ought to think about the role of data-creation in the economy, according to a fascinating new economics paper. We are all digital labourers, helping make possible the fortunes generated by firms like Google and Facebook, the authors argue. If the economy is to function properly in the future—and if a crisis of technological unemployment is to be avoided—we must take account of this, and change the relationship between big internet companies and their users.

Artificial intelligence (AI) is getting better all the time, and stands poised to transform a host of industries, say the authors (Imanol Arrieta Ibarra and Diego Jiménez Hernández, of Stanford University, Leonard Goff, of Columbia University, and Jaron Lanier and Glen Weyl, of Microsoft). But, in order to learn...

A new market for old and ugly fruit and vegetables takes shape

{kind=link}

NO ONE knows quite how much fruit and vegetable produce never reaches the grocery checkout till. A fifth perhaps—or maybe twice that—is judged to be beneath commercial standards. So it is put to use as animal-feed or compost, or simply thrown away in a landfill. This infuriates those appalled at waste. Their outrage, however, has not been enough to create for unwanted fruit and vegetable the kind of sophisticated market that exists for products with more obvious uses, such as securities, currencies, metals, oil and unsullied agriculture. That is starting to change.

At least two companies, Imperfect produce (whose logo is a misshapen potato that looks like a heart) and Hungry Harvest (whose slogan is “Rescued Produce. Delivered”), now provide boxes of subpar stuff directly to retail customers, one concentrating on the west coast of America, the other on the east. Another company, Full Harvest, has the wholesale market in its sights, linking...

Economists grapple with the future of the labour market

WHY is productivity growth low if information technology is advancing rapidly? Prominent in the 1980s and early 1990s, this question has in recent years again become one of the hottest in economics. Its salience has grown as techies have become convinced that machine learning and artificial intelligence will soon put hordes of workers out of work (among tech-moguls, Bill Gates has called for a robot tax to deter automation, and Elon Musk for a universal basic income). A lot of economists think that a surge in productivity that would leave millions on the scrapheap is unlikely soon, if at all. Yet this year’s meeting of the American Economic Association, which wound up in Philadelphia on January 7th, showed they are taking the tech believers seriously. A session on weak productivity growth was busy; the many covering the implications of automation were packed out.

Recent history seems to support productivity pessimism. From 1995 to 2004 output per hour worked grew at an annual average pace of 2.5%; from 2004 to 2016 the pace was just 1%. Elsewhere in the G7 group of rich countries, the pace has been slower still. An obvious explanation is that the financial crisis of 2007-08 led firms to defer productivity-boosting investment. Not so, say John Fernald, of the Federal Reserve Bank of San Francisco, and co-authors, who estimate that in America, the slowdown began in...

Peter Sutherland, former head of the GATT and the WTO, dies

{kind=link}

LIKE the showman he sometimes was, Peter Sutherland, on December 15th 1993, concluded seven years of torturous trade negotiations by banging a gavel. He received a standing ovation. Mr Sutherland, who died on January 7th, had an indispensable role in dragging the “Uruguay round” of trade talks to agreement. He did not know that this was to be the last such comprehensive, multilateral trade deal of his lifetime.

As director-general of the General Agreement on Tariffs and Trade and, on its founding, of the World Trade Organisation, the Irishman was the public face of bodies helping to integrate the global economy. The sobriquet “father of globalisation” was, at the time, a compliment. He remained proud of the WTO. In 2004 he wrote that “for the first time in history, the world can embrace a rules-based system for economic coexistence.”

Mr Sutherland, a lawyer by training, came to Geneva by way of the Irish attorney-general’s office and the European Union. Briefly in...

Bitcoin is no long the only game in crypto-currency town

IT STARTED as a joke. Dogecoin was launched in 2013 as a bitcoin parody, using as its mascot a Japanese shiba inu dog, a popular internet meme. The crypto-currency was never really used, except for tipping online, and one of its founders has called it quits. But recently its price has soared: on January 7th the dollar value of all Dogecoins in circulation reached $2bn, a sign of how crazy crypto-currency markets have become. It is also a reminder that, for all the focus on bitcoin, it is no longer the only game in town. Its market capitalisation now amounts to only about one-third of the crypto-market (see chart).

A new crypto-currency is born almost daily, often through an “initial coin offering” (ICO), a form of online crowdfunding. CoinMarketCap, a website, lists about 1,400 digital coins or tokens, including UFO Coin, PutinCoin, Sexcoin and InsaneCoin (worth $7m). Most are no more than curiosities, but by January 10th, around 40 had a market capitalisation of more than $...

Investment banks’ cull of company analysts brings dangers

{kind=link}

THEY are not extinct, nor even on the endangered-species list. But company analysts, once among the most prestigious professionals in the stockmarket, are being culled. New European rules, with the catchy name of MiFID2, have just dealt analysts another blow. A study by Greenwich Associates estimates that the budget for the research they perform may drop by 20% this year.

In their heyday in the late 1980s and early 1990s, analysts could make or break corporate reputations. A “buy” or “sell” recommendation from the leading two or three analysts in an industry could move a share price substantially. Fund managers, and many financial journalists, relied on analysts to spot those companies that were on a rising trajectory, and those where the accounts revealed signs of imminent trouble. And the best analysts were very well paid.

But that golden age was built on some rusty foundations. Analysts were well paid because they worked for the big investment banks. But those...

As China gets tough on pollution, will its economy suffer?

{kind=link}

LEO YAO thought he had nothing to fear from the environment ministry. Before, when its inspectors visited his cutlery factory, he says, they generated “loud thunder, little rain”. After warning him to clean up, they would, at worst, impose a negligible fine. Not so this time. In August dozens of inspectors swarmed over his workshop in Tianjin, just east of Beijing, and ordered production to be halted. His doors remain shut today. If he wants to go on making knives and forks, he has been told that he must move to more modern facilities in a less populated area.

Mr Yao’s company, which at its peak employed 80 people, is just one minor casualty in China’s sweeping campaign to reduce pollution. For years the government has vowed to go green, yet made little progress. It has flinched at reining in dirty industries, wary of the mass job losses that seemed likely to ensue. But in the past few months it has taken a harder line and pressed on with pollution controls, hitting coalminers, cement-makers...

As China gets tough on pollution, will its economy suffer?

LEO YAO thought he had nothing to fear from the environment ministry. Before, when its inspectors visited his cutlery factory, he says, they generated “loud thunder, little rain”. After warning him to clean up, they would, at worst, impose a negligible fine. Not so this time. In August dozens of inspectors swarmed over his workshop in Tianjin, just east of Beijing, and ordered production to be halted. His doors remain shut today. If he wants to go on making knives and forks, he has been told that he must move to more modern facilities in a less populated area.

Mr Yao’s company, which at its peak employed 80 people, is just one minor casualty in China’s sweeping campaign to reduce pollution. For years the government has vowed to go green, yet made little progress. It has flinched at reining in dirty industries, wary of the mass job losses that seemed likely to ensue. But in the past few months it has taken a harder line and pressed on with pollution controls, hitting coalminers, cement-makers...