The Economist - Finance and economics

Buying local is more expensive than it looks

{kind=link}

RANDY KULL, a businessman based in Illinois, sells traffic signs. His products have international appeal, with signs for anglophones (STOP), Spanish-speakers (ALTO) and horses (WHOA). But for some customers, he must stay local. When America’s Department of Transportation is involved, he must use American-made sign-mounting brackets, and fill in a form confirming their source. Mr Kull’s supplier in Arkansas is happy, but he himself is dubious. “We live in a global economy,” he scoffs. The weight of the evidence backs his instinctive scepticism.

To many, buying local seems sensible—wholesome, even. Keeping money close to home is supposed to foster thriving communities and generate jobs. To the administration of President Donald Trump, it is a source of national strength. Around the world, such sentiments are gaining ground. Global Trade Alert, a watchdog, has picked up 343 examples of new local-content requirements imposed since November 2008. In America, it estimates that the share...

In a pre-Brexit skirmish with the City, Eurex takes on LCH

{kind=link}

SEEN from the continent, it just isn’t right. LCH, a firm mostly owned by the London Stock Exchange (LSE), dominates the clearing of interest-rate derivatives. Each day it clears $3.4trn-worth, counting both sides of a trade. (The simplest variety is a swap of fixed and floating rates, allowing counterparties to reduce or increase their exposure to changes in rates.) In euro-denominated derivatives, the biggest category after dollars, LCH’s market share comfortably exceeds 90%, according to Clarus Financial Technology, a research firm.

Eurex, the derivatives arm of Deutsche Börse, owner of the Frankfurt Stock Exchange, wants to change that. So do European Union politicians and regulators, once Britain quits the EU. On November 20th Eurex’s clearing division said that so far around 20 banks, including lots of heavyweights, had joined a “partnership programme” to boost its interest-rate business. (The most notable absentees are Goldman Sachs and two big French banks, BNP Paribas and Société Générale.)

Though...

How to survive as a bank in Afghanistan

{kind=link}

ECONOMISTS think of the opportunity cost of money as one reason to hold a bank deposit: rather than skulk under a mattress, cash could earn interest. In volatile, war-torn Afghanistan, neither option appeals. Money has to be kept secure somehow, but a bad bank might make off with its depositors’ money. In 2010 Kabul Bank collapsed after a spree of insider loans to shareholders, including a brother of the then president. A central-bank bail-out cost nearly 7% of GDP. Much of the nearly $1bn stolen has not been recovered.

A bank that customers trust, though, is in a strong position. So Afghanistan International Bank (AIB) does not pay any interest on its deposits, says Anthony Barned, its British chief executive. AIB was set up by the Asian Development Bank and private investors in 2004, and is the largest private bank in Afghanistan, holding $790m in deposits, around one-fifth of the country’s deposit base. It is also the most profitable.

As the only private institution with a dollar-clearing facility with big...

Sustainable investment joins the mainstream

{kind=link}

IN 2008, when she was in her mid-20s and sitting on a $500m inheritance, Liesel Pritzker Simmons asked her bankers about “impact investing”. They fobbed her off. “They didn’t understand what I meant and offered to screen out tobacco,” recalls the Hyatt Hotels descendant, philanthropist and former child film star. So she fired her bankers and advisers and set up her own family office, Blue Haven Initiative. It seeks investments that both offer market-rate returns and have a positive impact on society and the environment. “Financially it’s sensible risk mitigation,” she says. “Our philanthropy becomes far more efficient if we don’t need to undo damage done in our investment management.”

Such ideas are gaining ground, particularly among the young. Fans of “socially responsible investment” (SRI) hope that millennials, the generation born in the 1980s and 1990s, will drag these concepts into the investment mainstream. SRI is a broad-brush term, that can be used to cover everything from...

Does Hong Kong’s Octopus card have too many tentacles?

{kind=link}

IN 1997, two months after Hong Kong reverted to Chinese sovereignty, it acquired a cutting-edge payment technology. People could rush through turnstiles with a wave of their colourful Octopus cards—stored-value cards pre-loaded with cash. Its latest advance, however, is risibly low-tech. On October 30th Octopus launched an extensible pole with a plastic hand to help drivers pay at toll booths. Critics of Hong Kong’s cautious approach to fintech snorted in derision. Meanwhile, a government official was quoted as blaming Octopus for stifling the city’s shift to cashlessness. Both criticisms are unfair. Hong Kongers enthusiastically embrace electronic payments and do well from the fierce competition between different platforms.

The Octopus card, designed for journeys on Hong Kong’s trains, buses, trams and ferries, soon stretched its tentacles into shops. In 2016 the company generated revenues of HK$956m ($122m) for its owners (mostly...

Wealth inequality has been widening for millennia

{kind=link}

THE one-percenters are now gobbling up more of the pie in America—that much is well known. This trend, though disconcerting, is not unique to the modern era. A new study, by Timothy Kohler of Washington State University and 17 others, finds that inequality may well have been rising for several thousand years, at least in some parts of the world. The scholars examined 63 archaeological sites and estimated the levels of wealth inequality in the societies whose remains were dug up, by studying the distributions of house sizes.

As a measure they used the Gini coefficient (a perfectly equal society would have a Gini coefficient of zero). It rose from about 0.2 around 8000BC in Jerf el-Ahmar, on the Euphrates in modern-day Syria, to 0.5 in around 79AD in Pompeii. Data on burial goods, though sparse, point to similar trends.

The researchers suggest agriculture is to blame. The nomadic lifestyle is not conducive to wealth accumulation. Only when humans switched to farming did...

Who needs America?

{kind=link}

REVIVING the original Trans-Pacific Partnership (TPP), a trade deal between 12 countries around the Pacific Rim, is technically impossible. To go into force, members making up at least 85% of their combined GDP had to ratify it. Three days into his presidency, Donald Trump announced that America was out. With 60% of members’ GDP gone, that deal was doomed.

But on November 11th, another began to rise in its place, crowned with a tongue-twisting new name: the Comprehensive and Progressive Agreement for the Trans-Pacific Partnership (CPTPP). Ministers from its 11 members issued a joint statement saying that they had agreed on its core elements, and that it demonstrated their “firm commitment to open markets”. The political symbolism was powerful. As America retreats, others will lead instead.

The CPTPP is still far from finished, however. This inconvenient truth is unsurprising. Resuscitating the deal without its biggest member was always going to be hard. Without America, uncomfortable concessions made in the old...

Fuelled by Middle East tension, the oil market has got ahead of itself

{kind=link}

ONLY one thing spooks the oil market as much as hot-headed despots in the Middle East, and that is hot-headed hedge-fund managers. For the second time this year, record speculative bets on rising oil prices in American and European futures have made the market vulnerable to a sell-off. “You don’t want to be the last man standing,” says Ole Hansen of Saxo Bank.

On November 15th, the widely traded Brent crude futures benchmark, which had hit a two-year high of $64 a barrel on November 7th, fell below $62. America’s West Texas Intermediate also fell. The declines coincided with a sharp drop across global metals markets, owing to concern about slowing demand in China, which has clobbered prices of nickel and other metals that had hit multi-year highs. (In a sign of investor nervousness after a sharp rally this year in global stock and bond markets, high-yield corporate bonds also weakened significantly this week.)

The reversal in the oil markets put a swift end to talk of crude shooting above $70 a barrel, which had...

Internship

Applications are invited for a Marjorie Deane internship in our New York bureau. The award is designed to provide work experience for a promising journalist or would-be journalist, who will spend three to six months at The Economist writing about economics, business and finance. Applicants are asked to write a covering letter and an article of no more than 500 words, suitable for publication in The Economist. Applications should be sent by December 14th to deaneinternny@economist.com.

The rich get richer, and millennials miss out

Early contender for the 2047 list

{kind=link}

BUOYANT financial markets meant that global wealth rose by 6.4% in the 12 months to June, the fastest pace since 2012. And the ranks of the rich expanded again, with 2.3m new millionaires added to the total, according to the Credit Suisse Research Institute’s global wealth report.

The report underlines the sharp divide between the wealthy and the rest. If the world’s wealth were divided equally, each household would have $56,540. Instead, the top 1% own more than half of all global wealth. The median wealth per household is just $3,582; if you own more than that, you are in the richest 50% of the world’s population.

America continues to dominate the ranks of millionaires with 43% of the global total. Both Japan and Britain had fewer dollar millionaires than they did in June 2016, thanks to declines in the yen and sterling. Emerging economies have been catching up in the millionaire stakes; they now have 8.4...

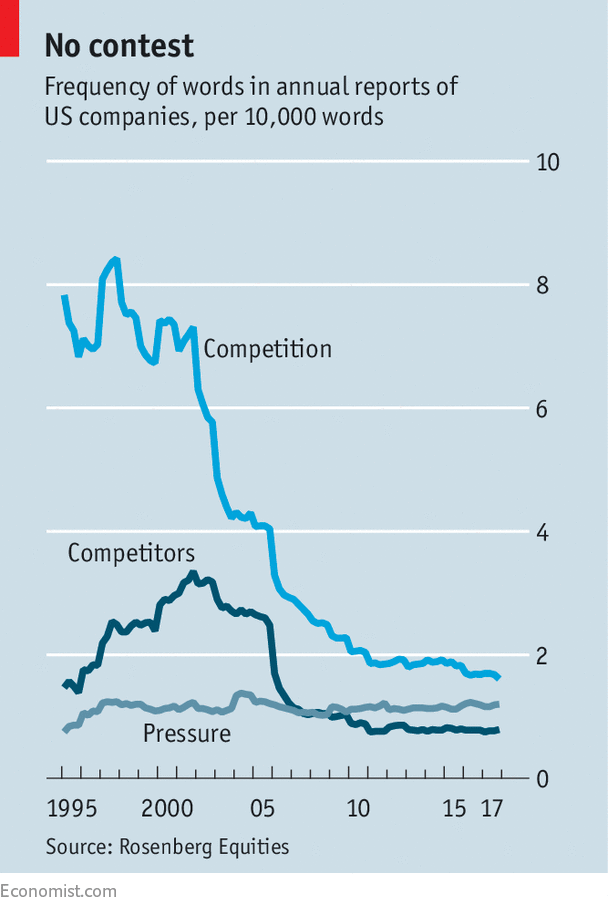

What annual reports say, or do not, about competition

{kind=link}

What explains the remarkable strength of corporate profits and the sluggish growth of real wages in recent years? One explanation is that industries are getting less competitive. Work by The Economist found that two-thirds of American industries were more concentrated in the hands of a few firms in 2012 than in 1997.

Research by AXA Investment Managers Rosenberg Equities into the language used in American annual reports points in the same direction. Sherlock Holmes famously talked of the significance of the dog that did not bark in the night. It may be similarly important that companies refer to rivals much less than they did; usage of the word “competition” in annual reports has declined by three-quarters since the turn of the century. Business is less cut-throat than it used to be.

ABP, a Dutch pension giant, is more admired abroad than at home

{kind=link}

EUROPE’S largest pension fund, a scheme for Dutch public-sector workers called ABP, is much feted abroad for its efforts in “sustainable” investing. At home, however, where it provides pensions to one in six families and manages nearly one-third of pension wealth, it is suffering a crisis of confidence.

By international standards, Dutch pensions are extremely generous overall, offering 96% of career-averagesalaries (adjusted for inflation), compared with an OECD mean of 63%. And they are solid. Thanks to mandatory, tax-deductible saving, the Dutch have stored up a collective pension pot of nearly €1.4trn ($1.6trn), roughly double GDP. Mercer, a consultancy, marks the country as second only to Denmark in a global ranking of schemes.

Yet Dutch people’s faith in their pensions has sunk as low as their trust in banks and insurers. In March a political party for older voters, 50+, won four seats in the Dutch parliament, largely thanks to its promise to “stop the pension raid”. ABP’s own members mark it at just 5.9 out...

Timelier provisions may make banks’ profits and lending choppier

{kind=link}

IN THE first quarter of 2018 thousands of banks will look a little less profitable. A new international accounting standard, IFRS 9, will oblige lenders in more than 120 countries, including the European Union’s members, to increase provisions for credit losses. In America, which has its own standard-setter, IFRS 9 will not be applied—but by 2019 banks there will also have to follow a slightly different regime.

The new rule has its roots in the financial crisis of 2007-08, in the wake of which the leaders of the G20 countries declared that accounting standards needed an overhaul. Among their other shortcomings, banks had done too little, too late, to recognise losses on wobbly assets. Under existing standards they make provisions only when losses are incurred, even if they see trouble coming. IFRS 9, which comes into force on January 1st, obliges them to provide for expected losses instead.

Under IFRS 9 bank loans are classified in one of three “stages”. When a loan is made—stage one—banks must make a provision...

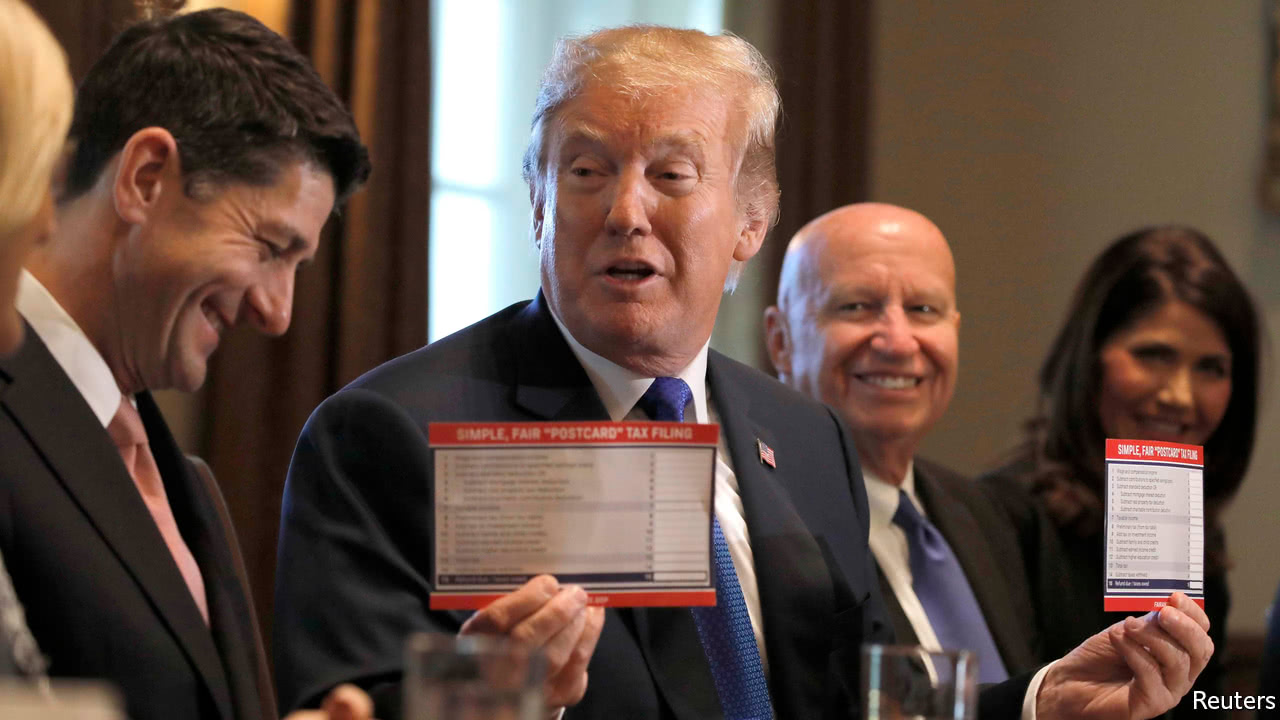

What is the purpose of tax reform?

{kind=link}

IF MAKING America great again is the aim, you could do worse than bring back the economic growth rates of the late 1990s. President Donald Trump’s team reckons that the Republican tax plan making its way through Congress will do just that. “We are creating a model that creates economic growth in this country,” says Gary Cohn, the director of Mr Trump’s National Economic Council. Kevin Hassett, who runs the Council of Economic Advisers, reckons the bill should push growth above 4% per year.

Such heights are not beyond the realm of possibility, but if America reaches them tax reform will have little to do with it. That is not because of the specifics of the plan. Rather, it reflects an underappreciated reality: tax reform can accomplish many things, but raising long-run growth is not generally among them.

Most assessments of the Republican tax proposals, like most analyses of most tax plans, conclude their effects on growth will be small. The Penn Wharton Budget Model, a non-partisan public-policy initiative,...

What five years of Abenomics has and has not achieved

{kind=link}

IN TOKYO’S Iidabashi district, north of the Imperial Palace, young salarymen and women gather after work to enjoy grilled chicken and a drink at Torikizoku, a chain of budget restaurants. They tap out their orders on touch-screen terminals, which the company has installed on many tables in an effort to economise on waiters, whose wages are hard to contain. Last month the company was forced to raise its price by over 6%, to ¥298 (about $2.60) plus tax, for two skewers of locally reared chicken yakitori. It was the firm’s first price increase in 28 years.

Chicken skewers are not commonly seen as a macroeconomic indicator. But Torikizoku’s decision exemplifies the underlying logic of “Abenomics”, a campaign to revive Japan’s economy, named after Shinzo Abe, its prime minister. His economic strategy aimed to stimulate spending and investment through vigorous monetary easing. That would create jobs, driving up wages. Higher wages, in turn, would push up prices. Success would be measured by the defeat of deflation, which had...

Criticism of index-tracking funds is ill-directed

{kind=link}

INDEX funds were devised in the 1970s as a way of giving investors cheap, diversified portfolios. But they have only become very popular in the past decade. Last year more money flowed into “passive” funds (those tracking a benchmark like the S&P 500) than into “active” funds that try to pick the best stocks.

In any other industry, this would be universally welcomed as a sign that innovation was coming up with cheaper products to the benefit of ordinary citizens. But the rise of index funds has provoked some fierce criticism.

Two stand out. One argues that passive investing is, in the phrase of analysts at Sanford C. Bernstein, “worse than Marxism”. A key role of the financial markets is to allocate capital to the most efficient companies. But index funds do not do this: they simply buy all the stocks that qualify for inclusion in a benchmark. Nor can index funds sell their stocks if they dislike the actions of the management. The long-term result will be bad for capitalism, opponents argue.

A...

Activist shareholders take on the London Stock Exchange

{kind=link}

ACTIVIST hedge funds like Elliott Management, Cevian Capital or The Children’s Investment Fund (TCI) are famed for pushing for change at the companies they buy into. A favoured tactic is to install a new chief executive at a floundering firm. So it is odd to find a fund lobbying for an existing boss to stay on, as TCI has done in a spat with the London Stock Exchange (LSE).

In over eight years at the LSE, Xavier Rolet has transformed it from a share-trading venue to a clearing and data-services powerhouse, through acquisitions such as Russell, an index-maker, and a majority stake in LCH, a clearing-house. His hope of merging with the LSE’s big German rival, Deutsche Börse, fell through, largely because of Britain’s vote to leave the EU. But Mr Rolet remains widely respected. So eyebrows were raised when the LSE’s announcement on October 19th that Mr Rolet would leave in 2018 gave no reason.

In a fiery letter penned on...

Regulators begin to tackle the craze for initial coin offerings

{kind=link}

“I’M GONNA make a $hit t$n of money on August 2nd on the Stox.com ICO.” Written in July on Instagram, these words made Floyd Mayweather, a boxer, the first big celebrity to endorse an “initial coin offering”, a form of crowdfunding that issues cryptographic coins, or “tokens”. Stox, an online prediction market, went on to raise more than $30m, some of which seems to have gone directly into Mr Mayweather’s pocket. Other VIPs, including Paris Hilton, a socialite, followed suit and endorsed ICOs. But this source of easy cash may now be drying up: on November 1st America’s Securities and Exchange Commission (SEC) warned that such promotions may be unlawful, if celebrities fail to disclose what they receive in return.

The endorsements and the SEC’s attempt to rein them in are the latest episodes of token mania. Virtually unknown a year ago, ICOs are now more celebrated than initial public offerings (IPOs), the conventional way of floating a firm. Over the past 12 months $3.3bn has been...

ING, a Dutch bank, finds a winning digital strategy

{kind=link}

GERMANY’S third-biggest retail bank has no branches. It is also Dutch. And it is highly profitable. ING-DiBa, an online bank owned by ING, the Netherlands’ biggest lender, looks after €133bn ($154bn) of deposits for over 8m customers. In a fragmented market—most Germans entrust their savings to small, local banks—that means a share of around 6%. ING-DiBa’s lack of branches keeps costs down, allowing it to resist charging for current accounts and offer savers a tad more than rivals, despite a recent cut; and it has won a name for good service in a country not renowned for it. While other banks struggle after years of ultra-low interest rates, ING-DiBa thrives. Its return on equity exceeds 20%.

ING as a whole is in fair shape, too. On November 2nd it reported net third-quarter earnings of €1.4bn, slightly more than a year earlier. The group’s return on equity was a healthy 11%, nearly two percentage points up. Since 2014 the number of “primary” customers (with an active current account and another product) has climbed by 25%, to...

America’s Republicans take aim at mortgage subsidies

{kind=link}

IN THE 1980s Margaret Thatcher and Ronald Reagan were both proud of their efforts to expand home ownership. In Britain, Thatcher presided over a fire sale of state-owned homes to tenants. In America, Reagan deregulated financial markets and expanded mortgage lending. At the time both countries provided generous mortgage-related tax breaks, making it easier to flog homes to the masses.

Britain’s 1980s housing boom turned to bust; the mortgage subsidies that helped to fuel it were abolished. America still subsidises mortgages to the tune of $64bn a year, by allowing homeowners to deduct interest costs from their tax liabilities. But a tax plan unveiled by Republicans on November 2nd proposes to limit the subsidy.

Twelve European Union countries also include some form of mortgage-interest deduction (MID) in their tax code. The average European subsidy, however, is around a tenth of America’s—about 0.05% of GDP. The Netherlands is much the most generous, at 2% of GDP.

...

- « primera

- ‹ anterior

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- siguiente ›

- última »