The Economist - Finance and economics

After a bumper 2017, will 2018 be kind to the financial markets?

{kind=link}

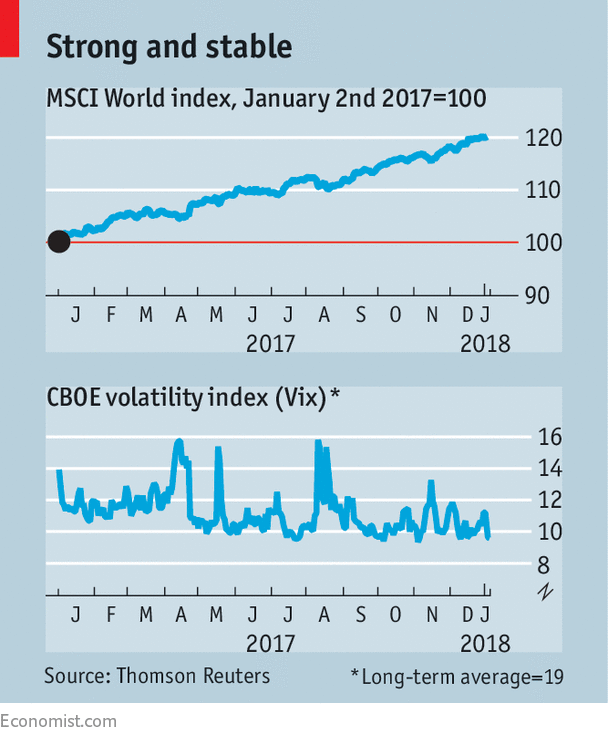

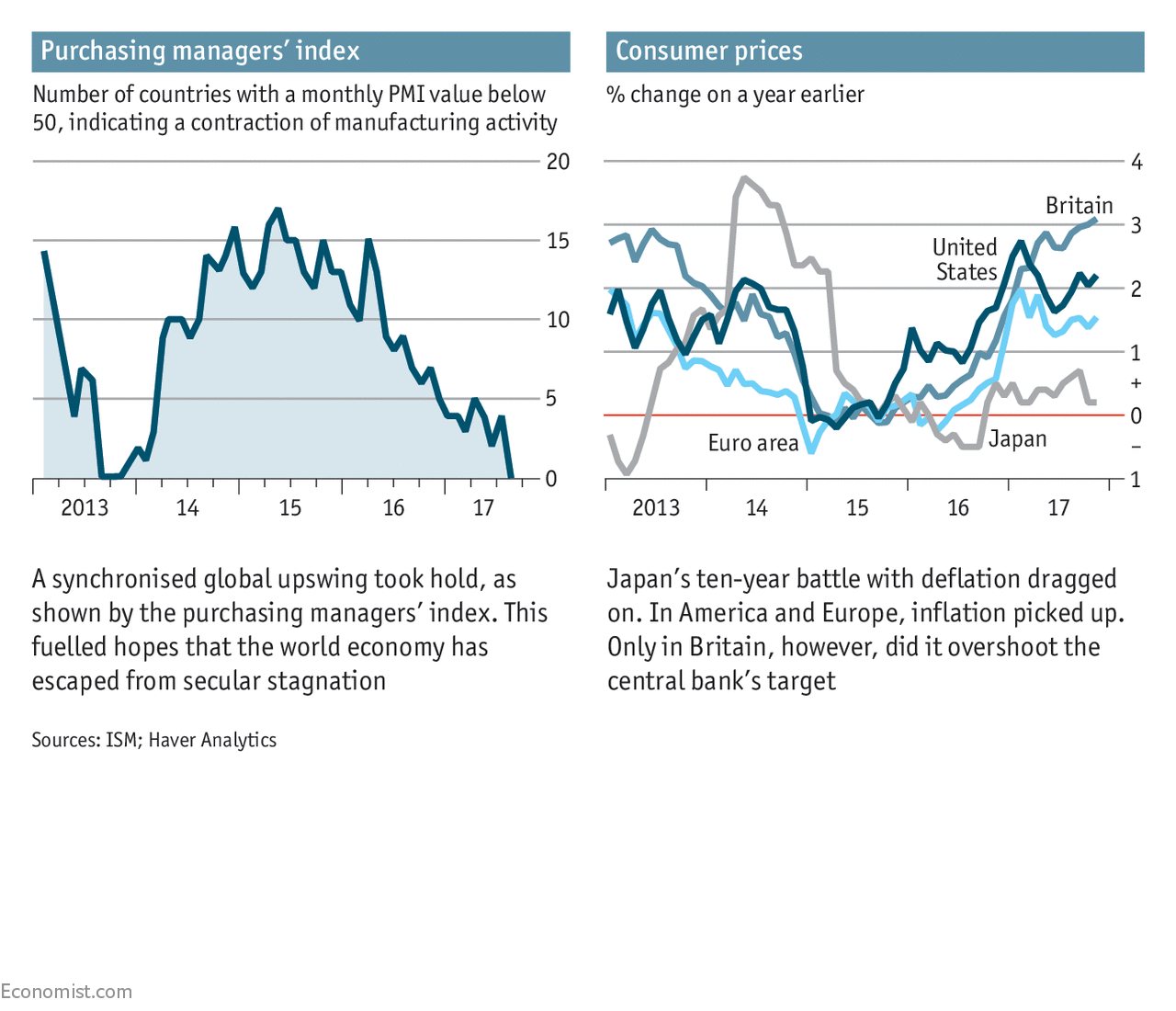

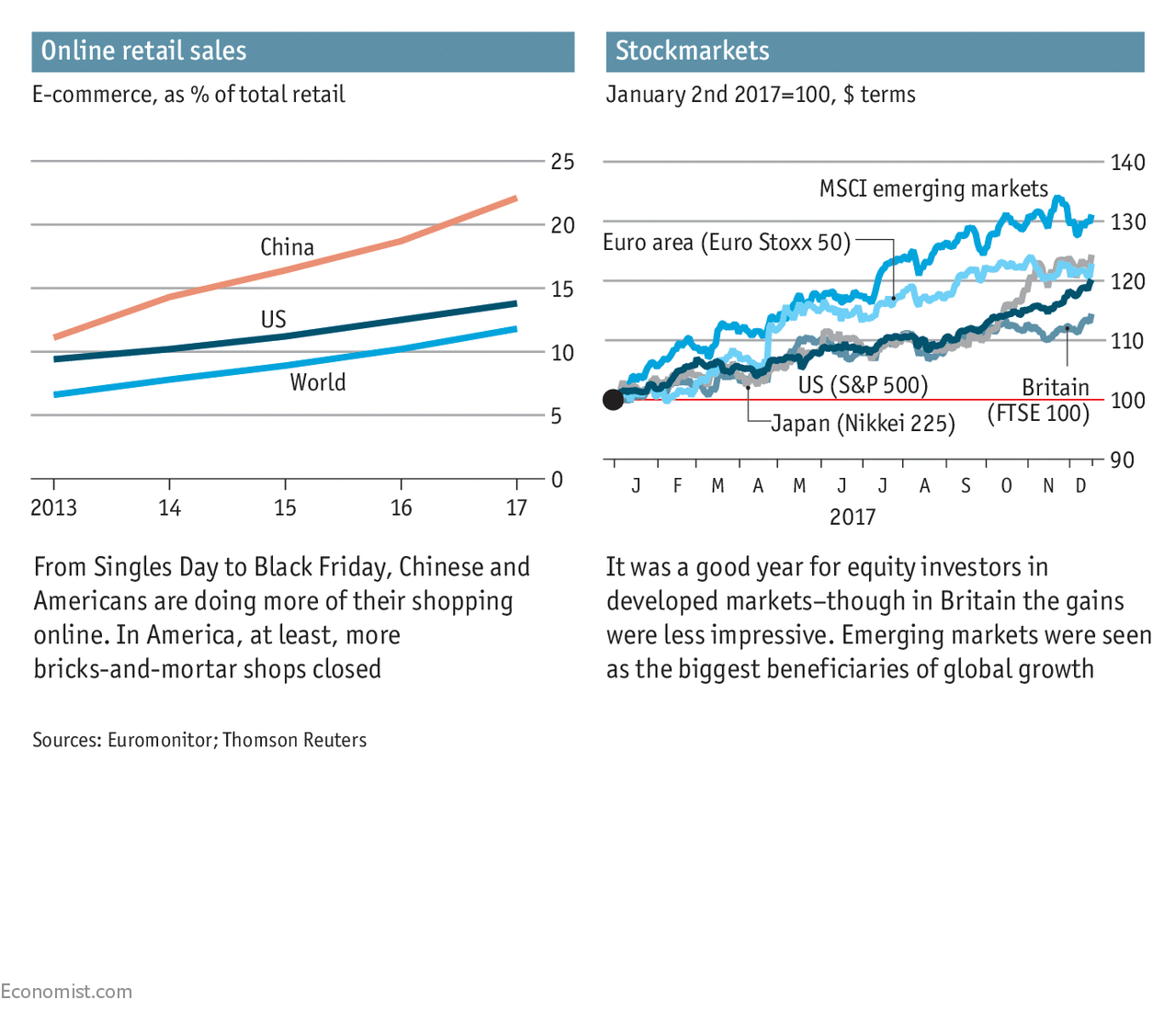

AFTER a bumper year for financial markets in 2017, can 2018 be anything like as good? Much will depend on the global economy. The rally in stockmarkets stretches back almost two years, to the point when worries about an era of “secular stagnation” started to diminish.

{kind=link}

The first pieces of economic data to be published in January—the purchasing managers’ indices (PMI) for the manufacturing sector—were pretty upbeat. In the euro zone the index recorded its highest level since the survey began in 1997. China’s PMI was stronger than expected, and America’s index showed new orders at their highest...

A bond dispute threatens the future of Islamic finance

{kind=link}

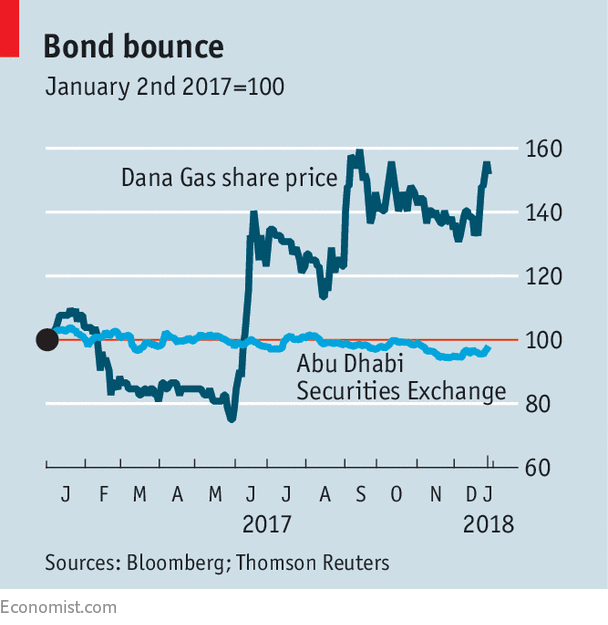

STOCKMARKETS in the Gulf do not observe Christian holidays, but still had a generally quiet day on December 25th. Shares in Dana Gas, an exploration business listed in Abu Dhabi, however, did make some noise, leaping by 13.2% on Christmas Day, to complete a buoyant six months for the stock (see chart). The surge may owe something to the company’s recent arbitration victory against the regional government of Iraqi Kurdistan, over $2bn it and its consortium partners are owed in overdue payments. But it also hints at shareholders’ belief that Dana will not be forced soon to satisfy its own creditors. They have been up in arms since the firm refused to honour a $700m Islamic bond, or sukuk, that matured in October.

{kind=link}

Many happy returns: new data reveal long-term investment trends

{kind=link}

DATA-GATHERING is the least sexy part of economics, which is saying something. Yet it is also among the most important. The discipline is rife with elaborate theories built on assumptions that turned out to be false once someone took the time to pull together the relevant data. Accordingly, one of the most valuable papers produced in 2017 is an epic example of data-retrieval: a piece of research that spells out the rates of return on important asset classes, for 16 advanced economies, from 1870 to 2015. It is fascinating work, a rich seam for other economists to mine, and a source of insight into some of today’s great economic debates.

Rates of return both influence and are influenced by the way firms and households expect the future to unfold. They therefore find their way into all sorts of economic models. Yet data on asset returns are incomplete. The new research, published as an NBER working paper in December 2017, fills in quite a few gaps. It is the work of five economists: Òscar Jordà...

America’s bank profits take a hit from tax reform

{kind=link}

WHEN Donald Trump won America’s presidential election 14 months ago, banks’ share prices leapt. One reason for that was the prospect of lower corporate taxes, which would both benefit banks directly and (investors hoped) ginger up the economy. Like Mr Trump’s legislative agenda, their shares were becalmed for much of 2017, but they perked up late in the year when the Tax Cuts and Jobs Act looked likely to become law—as it duly did when the president signed it on December 22nd.

Yet several banks expect the act to make deep dents in fourth-quarter profits. On December 28th Goldman Sachs said it was braced for a $5bn hit. A week before, Bank of America (BofA) announced a $3bn write-down. Early in the month, on fairly accurate assumptions about the law’s final form, Citigroup put the cost at a whopping $20bn. Foreign banks are also assessing the damage: £1bn ($1.4bn), says Barclays; SFr2.3bn ($2.4bn), reckons Credit Suisse.

These one-off hits have two main causes. First...

Europe’s sprawling new financial law enters into force

{kind=link}

AFTER years of rule-drafting, industry lobbying and plenty of last-minute wrangling, Europe’s massive new financial regulation, MiFID 2, was rolled out on January 3rd. Firms had spent months dreading (in some cases) or eagerly awaiting (in others) the “day of the MiFID” when the law’s new reporting requirements would enter into force. One electronic-trading platform, Tradeweb, even gave its clients a “MiFID clock” to count down to it.

Apprehension was understandable. The new EU law, the second iteration of the Markets in Financial Instruments Directive (its full, unwieldy name), affects markets in everything from shares to bonds to derivatives. It seeks to open up opaque markets by forcing brokers and trading venues to report prices publicly, in close to real time for those assets deemed liquid. It also requires them to report to regulators up to 65 separate data points on every trade, with the aim of avoiding market abuse.

The changes are greatest for markets, like those in...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Intangible assets are changing investment

{kind=link}

WHEN you work as an equity analyst at an investment bank, your task is clear. It is to comb all the statements made by corporate executives, to scour the industry trends and arrive at an accurate forecast of the company’s profits. Achieve this and your clients will be happy and your bonus cheque will have many digits.

But is all this effort worthwhile? Not as much as it used to be, according to Feng Gu and Baruch Lev, writing in a recent issue of Financial Analysts Journal*. The authors imagined that investors could perfectly forecast the next quarter’s earnings for all companies. They then assumed that investors bought all the stocks that they expected to meet or beat the consensus of analysts’ forecasts; and that investors could short (ie, bet on a declining price) the stocks of those that were predicted not to reach their estimates. They made their investment two months before the end of a quarterly reporting period and got out of their positions one month after the...

Countries rarely default on their debts

{kind=link}

VENEZUELA is an unusual country. It is home to the world’s largest reserves of oil and its highest rate of inflation. It is known for its unusual number of beauty queens and its frightening rate of murders. Its bitterest foe, America, is also its biggest customer, buying a third of its exports.

In defaulting on its sovereign bonds last month (it failed to pay interest on two dollar-denominated bonds by the end of a grace period on November 13th), Venezuela is also increasingly unusual. The number of governments in default to private creditors fell last year to its lowest level since 1977, according to the Bank of Canada’s database. Of the 131 sovereigns tracked by S&P Global, a rating agency, Mozambique is the only other country in default, having missed payments on its Eurobond (and failed to make good on guaranteed loans to two state-owned enterprises). Walter Wriston, a former chairman of Citibank, earned ridicule for once declaring that “countries don’t go bust”. But they don’t much...

Have yourself a dismal Christmas

{kind=link}

ONLY an economist would think to ask whether Christmas is efficient. In 1993 Joel Waldfogel, then a professor at Yale University, turned a lunchtime conversation with colleagues into a paper entitled “The deadweight loss of Christmas”, which argued that, no, it is not. That gift-giving might actually be bad is the kind of opinion which breeds a deep mistrust of economists—loathing is perhaps too strong—among those not schooled in the dismal science. It is also just the sort of analytical insight on which economists pride themselves: counterintuitive, irreverent and interesting. But they should perhaps be less pleased with themselves. The way they think about the most festive time of the year reveals something important about the shortcomings of the field’s approach to human behaviour.

Mr Waldfogel’s notion was a clever one. Massive amounts of money are spent on holiday presents; it makes sense to ask whether such spending leaves the world better off. In buying gifts, people do their best to...

A decade after it hit, what was learnt from the Great Recession?

TEN years ago this month, America entered the “Great Recession”. A decade on, the recession occupies a strange space in public memory. Its toll was clearly large. America suffered a cumulative loss of output estimated at nearly $4trn, and its labour markets have yet to recover fully. But the recession was far less bad than it might have been, thanks to the successful application of lessons from the Depression. Paradoxically, that success spared governments from enacting bolder reforms of the sort that might make the Great Recession the once-a-century event economists thought such calamities should be.

Good crisis response treats its symptoms; the symptoms of a disease, after all, can kill you. On that score today’s policymakers did far better than those of the 1930s. Government budgets have become a much larger share of the economy, thanks partly to the rise of the modern social safety net. Consequently, public borrowing and spending on benefits did far more to stabilise the economy than they did during the Depression. Policymakers stepped in to prevent the extraordinary collapse in prices and incomes experienced in the 1930s. They also kept banking panics from spreading, which would have amplified the pain of the downturn. Though unpopular, the decision to bail out the financial system prevented the implosion of the global economy.

But the success of...

The markets’ apparent calm over Brexit is deceptive

FOR all the sound and fury of the Brexit negotiations, it has seemed at times as if the financial markets have been barely affected. But as with the swans that glide on the Thames, a serene surface conceals some frantic paddling underneath.

The pound is the most reliable indicator of the Brexit mood. A rule of thumb is that, if the headlines point to a “hard” Brexit (creating trade barriers with the EU), sterling will fall; signs of a “soft” Brexit (something that is close to the current relationship) will cause it to rise.

But some feedback processes are at work. The big fall in the pound in the immediate aftermath of the referendum has led to a gradual rise in imported inflation. The annual inflation rate hit 3.1% in November, requiring Mark Carney, governor of the Bank of England, to write to Philip Hammond, the chancellor, to explain why the target (of 2%) had been missed. The bank has already raised interest rates once. More rises may follow, and expectation of such rises supports the pound.

The need for monetary tightening is not simply a result of higher import costs, which might prove temporary. More worryingly, the Bank thinks that the trend rate of growth of the British economy has fallen (a view it shares with the Office for Budget Responsibility, the government’s forecasting arm). In part, this is because Britain faces a more...

Will America’s economy overheat in 2018?

{kind=link}

USUALLY politicians pretend that good economic news on their watch is no surprise. But America’s recent growth figures have been so positive that even the administration of President Donald Trump has allowed itself to marvel. “It’s actually happening faster than we expected,” mused Mick Mulvaney, the White House budget chief, in September, after growth rose to 3.1% in the second quarter. (Mr Trump in fact came to office promising 4% growth, but the goal now seems to be 3%.) Mr Mulvaney warned that hurricanes would soon bring growth back down. Instead, in the third quarter, it rose to 3.3%—a figure celebrated with more conviction. The administration’s initial caution was wise: quarterly growth figures are volatile, and few economists expect growth above 3% to carry on for long. Yet there is no denying that the economy is in rude health.

In part, that reflects the strength of the global economy. But it is also the culmination of a years-long trend. As politics has consumed America’s attention...

Bitcoin-futures contracts create as many risks as they mitigate

OFTEN promoted as a way of mitigating risk, futures contracts are frequently more like new ways of gambling. That was true of a close precursor to the instrument, introduced in the Netherlands in 1636, linked to the hot investment of the day—tulip bulbs. Likewise the world’s first two futures contracts linked to bitcoin. One launched on the Chicago Board Options Exchange (CBOE) on December 10th; the other was due to follow a week later on the Chicago Mercantile Exchange (CME).

As bitcoin’s price has soared to new highs (see chart), holders may be happy to have a way to hedge their exposure at last. But for many, the contracts are just another way in. Both contracts settle in cash (ie, for the difference between the agreed price and the actual spot price). No exchange of bitcoin is needed; similarly, in the Dutch precedent, no bulbs were involved.

Early trading on the CBOE certainly suggests a speculative market. In the first few hours, prices rose so quickly that trading twice had to be suspended. The contract has so far traded at a significant premium, of up to $2,000, to the spot price. This suggests there are more buyers than sellers—even though selling in the futures market offers a way to bet against bitcoin.

...

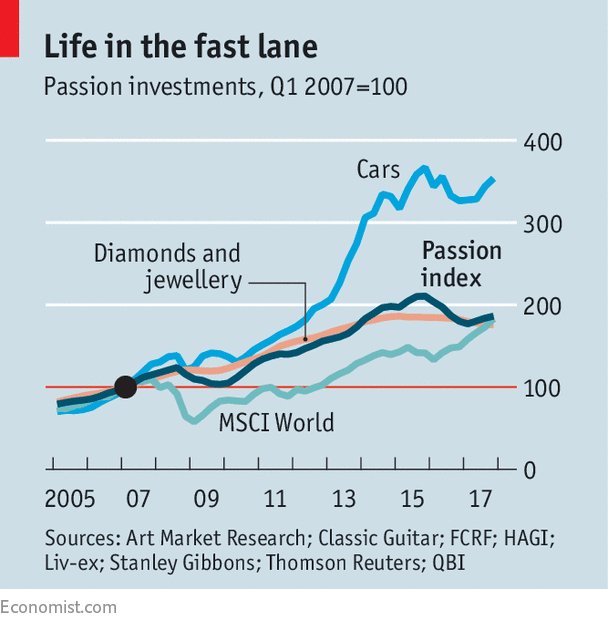

Cars, jewels, wine and watches have been good investments

{kind=link}

DIAMONDS, they say, are for ever. They can be pricey, too. On December 5th 173 lots of jewels auctioned by Sotheby’s raised $54m. They included several pieces belonging to Sean Connery, known for playing James Bond. The following day a car favoured by Bond, the Aston Martin DB5, was auctioned for $2.7m. It was among 24 classic vehicles that together fetched $45m. The sales in New York last week by the world’s two biggest auction houses, Sotheby’s and Christie’s, also involved fine wines, watches and other luxuries. Between them they sold $200m-worth.

The Economist has compiled price indices for many of these items—diamonds, classic cars, fine wine, art, watches and other curios—and grouped them in a “passion” index. The index is weighted according to the holdings of high-net-worth individuals (HNWI)—defined as people with more than $1m of investable assets—as reported by Barclays. Our passion index has dropped by 2% a year, on average, for the past three years. But since...

China’s leading economists are in high demand and short supply

{kind=link}

EVERGRANDE, a Chinese property firm, is a big spender. It was until recently the country’s most indebted developer. It also owns a football club with one of the highest payrolls in China. It has extended its largesse to a new field: economics. Having founded an economic-research institute, Evergrande last month poached Ren Zeping, a star analyst with a big brokerage, to serve as its first chief economist. His annual salary of 15m yuan ($2.3m) is, based on available information, the highest ever for an economist in China. Not bad for a country where forecasting the official growth figures accurately has for years required little more research than reading the official growth targets.

Yet Evergrande is not alone in splashing cash in China, whether in property, football or, lately, economics. Competition for the best—or, rather, best-known—economists is fierce. The past half year alone has resembled a frenzied transfer window for their services. Besides Mr Ren, half a dozen other...

The revised Basel bank-capital standards are complete at last

{kind=link}

HOWEVER long a storm lasts, clearing up takes longer. On December 7th Mario Draghi, president of the European Central Bank and head of the committee that approves global bank-capital standards, declared that revisions to Basel 3, the version drawn up after the financial crisis of 2007-08, were complete. The overhaul of the previous rules, which were blown away in the tempest, began eight years ago. The revised set, informally called Basel 4, will not take full effect until 2027.

That lengthy period of adjustment is one way in which Basel 4 is less demanding than banks, notably in Europe, had feared. Several other tweaks mean that the standards banks must eventually meet will be less exacting than first proposed. Already forced to bolster their balance-sheets with lots more equity—of which the crisis showed them to be woefully short—banks may deny that they have got off lightly. But they probably have.

Basel 4 was supposed to be settled a year ago. It wasn’t, because of a row...

The WTO remains stuck in its rut

{kind=link}

“THERE is life after Buenos Aires,” soothed Susana Malcorra, chair of the 11th ministerial meeting of the World Trade Organisation (WTO). Multilateralism may not be dead, but it has taken a kicking. Expectations were low as the meeting began in the Argentine capital. They sank even lower as it progressed. Delegates failed to agree on a joint statement, let alone on any new trade deals.

Many arrived with a culprit already in mind. Robert Lighthizer, the United States Trade Representative, was the face of an administration that is both questioning the benefits of multilateralism and jamming the WTO’s process of settling disputes. As negotiations progressed, some delegates groused that American leadership was lacking. Some even speculated that the Americans might be happy if multilateral talks foundered. What better proof, after all, that the system is broken?

Ms Malcorra, without mentioning the Americans by name, warned against creating scapegoats out of those who...

Oil and gas supply disruptions ripple around the world

{kind=link}

CALL it the hydrocarbon equivalent of the butterfly effect. As oil and gas supplies tighten during the northern winter, disruptions as remote as a hairline fracture on a piece of Scottish pipeline, and an explosion in an Austrian natural-gas plant, have repercussions felt around the world.

Start with the pipeline. After Ineos, a chemicals company, detected a growing crack on a piece of pipe near Aberdeen, on December 11th it said it would shut the main Forties pipeline carrying North Sea oil and gas to Britain for weeks. The suspension of a pipeline carrying 450,000 barrels a day (b/d) of crude, in a global market of almost 98m b/d, would not normally be disruptive. Yet Brent crude, the benchmark for pricing much of the world’s seaborne crude, is itself partly priced on the flow of crude from 80 fields that feed the Forties pipeline, magnifying the impact.

Futures prices for Brent crude delivered in February and March...

Hedge funds embrace machine learning—up to a point

{kind=link}

ARTIFICIAL intelligence (AI) has already changed some activities, including parts of finance like fraud prevention, but not yet fund management and stock-picking. That seems odd: machine learning, a subset of AI that excels at finding patterns and making predictions using reams of data, looks like an ideal tool for the business. Yet well-established “quant” hedge funds in London or New York are often sniffy about its potential. In San Francisco, however, where machine learning is so much part of the furniture the term features unexplained on roadside billboards, a cluster of upstart hedge funds has sprung up in order to exploit these techniques.

These new hedgies are modest enough to concede some of their competitors’ points. Babak Hodjat, co-founder of Sentient Technologies, an AI startup with a hedge-fund arm, says that, left to their own devices, machine-learning techniques are prone to “overfit”, ie, to finding peculiar patterns in the specific data they are trained on that do not hold up...

A full-scale Venezuelan default could push up oil prices

{kind=link}

ON NOVEMBER 30th, as oil tsars from the Organisation of the Petroleum Exporting Countries (OPEC) and Russia met in Vienna, Venezuela’s former oil minister, Eulogio del Pino, once one of their number, was seized by armed guards at dawn in Caracas, and taken to jail. His arrest was not publicly acknowledged in Vienna. His replacement, Manuel Quevedo, a general in the national guard, attended OPEC and was received with the usual deference.

Also unmentioned was how Venezuela, embroiled in a massive, messy debt default, is doing plenty of OPEC’s dirty work. Since November 2016, when OPEC first agreed with Russia to cut output to push up oil prices, Venezuela’s has fallen by 203,000 barrels a day (b/d), to 1.86m b/d in October. That is more than twice the cut it agreed with OPEC of 95,000 b/d.

If its production continues to fall—some analysts say it could be down to 1.6m b/d in 2018—it could either drive up oil prices...

- « primera

- ‹ anterior

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- siguiente ›

- última »