The Economist - Finance and economics

Europe is seeing more collective lawsuits from shareholders

{kind=link}

LIKE the ghosts that haunted Ebenezer Scrooge, the scandals of years past—summoned up by angry shareholders—will not let companies rest. In Britain this year, the Royal Bank of Scotland (RBS) paid £900m ($1.2bn) to settle a long-running investor lawsuit related to the bank’s behaviour at the time of the financial crisis of 2007-08. Also in Britain, Lloyds Banking Group faces litigation. And it is not just banks. Investors in Britain sued Tesco, a supermarket chain, for losses caused by an accounting scandal in 2014. In Germany and the Netherlands investors are seeking compensation from Volkswagen (VW), a carmaker, for failing to disclose its manipulation of diesel-emissions tests.

Securities litigation is on the rise in Europe for two main reasons. The first is that America is less hospitable than it was to such cases. Until 2010 harm suffered by foreign investors could be included in American lawsuits. That changed with a Supreme Court ruling on Morrison v National...

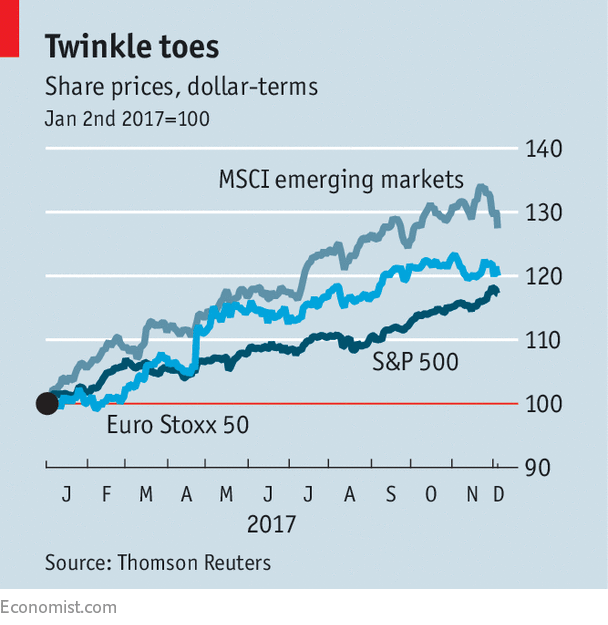

The markets believe in Goldilocks

ANOTHER week, another record. The repeated surge of share prices on Wall Street is getting monotonous. The Dow Jones Industrial Average has passed another milestone—24,000—and the more statistically robust S&P 500 index is up by 17% so far this year. Emerging markets have performed even better, as have European shares in dollar terms (see chart).

{kind=link}

Political worries about trade disputes, the potential for war with North Korea and the repeated upheavals in President Donald Trump’s White House: all have caused only temporary setbacks to investors’ confidence. No wonder the latest quarterly report of the Bank for International Settlements asked whether markets are complacent, noting that “according to traditional valuation gauges that take a long-term view, some stockmarkets did look frothy”, and pointing out that “some froth was also present in corporate-credit markets”.

The authors of the BIS report are not the only ones to worry that markets look expensive. The most recent survey...

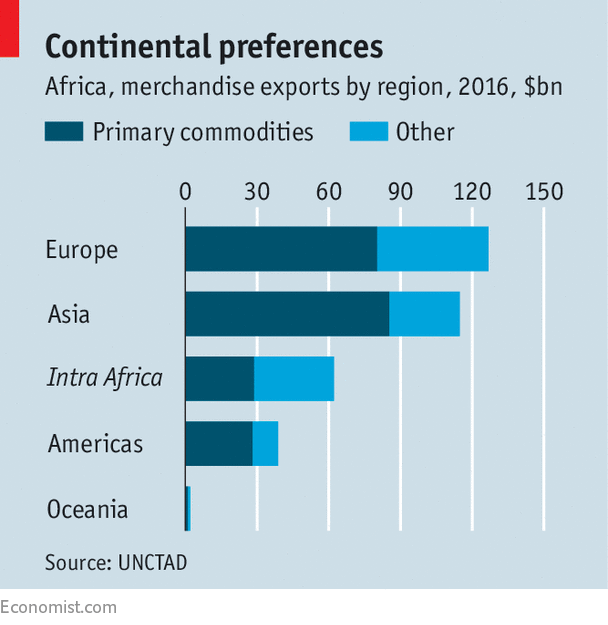

African countries are building a giant free-trade area

“AFRICA must unite,” wrote Kwame Nkrumah, Ghana’s first president, in 1963, lamenting that African countries sold raw materials to their former colonisers rather than trading among themselves. His pan-African dream never became reality. Even today, African countries still trade twice as much with Europe as they do with each other (see chart). But that spirit of unity now animates a push for a Continental Free-Trade Area (CFTA), involving all 55 countries in the region. Negotiations began in 2015, aimed at forming the CFTA by the end of this year. In contrast to the WTO, African trade talks are making progress.

{kind=link}

At a meeting on December 1st and 2nd in Niamey, the capital of Niger, African trade ministers agreed on final tweaks to the text. Heads of state will probably sign it in March, once an accompanying protocol on goods has been concluded (agreement on services has already been reached). But trade barriers will not tumble overnight. The CFTA will come into force only when 15 countries have...

China takes on the EU at the WTO

NOT all trade tension is made in America. China is suing the European Union at the World Trade Organisation (WTO). Hearings began this week. China thinks it deserves treatment as a “market economy”. The EU, supported by America, disagrees. As they lock horns, each side sees the other as breaking a promise.

China’s entry into the WTO in 2001 was part of a grand bargain. In return for market access, it promised economic reform. The deal laid out unusually strict terms. Any members’ exports can face anti-dumping duties if sold too cheap. But China’s accession agreement allowed others to erect stronger defences, and assume that it was a non-market economy when calculating the “fair” duty—using third-country prices for comparison. In practice this meant higher tariffs.

China expected this treatment to be temporary and expire after 15 years. But as the deadline loomed and the share of imports covered by anti-dumping duties rose (see chart), the EU and America balked at the idea of giving up their trade defences. On December 4th the EU approved new rules to drop the label of “non-market economy”. But it will still apply third-country pricing on a case-by-case basis. Mei Xinyu of the Chinese Academy of International Trade and Economic Co-operation, an official body, calls this “a trick that avoids calling China a non-market economy”.

...

Contraception does even more good in poor countries than thought

{kind=link}

FEW tasks in developing countries are as tricky—or as important—as convincing parents to keep their daughters in school longer. One way of doing so is to make contraceptives available, concludes a new working paper by Kimberly Singer Babiarz at Stanford University and four other researchers.

Conducted in Malaysia, the study used a happy coincidence of surveys going back decades and family-planning programmes rolled out in a way that made it possible to measure their effect. Starting in the 1960s, these programmes were introduced in some areas a few years earlier than in others. So researchers could compare what happened to girls in areas where contraceptives became available when they were very young with girls from the same cohorts in areas with no contraceptives.

The girls in places with contraceptives stayed in school six months longer, or about a year longer if they were born after the programmes began. Similar effects have been...

Are digital distractions harming labour productivity?

{kind=link}

FOR many it is a reflex as unconscious as breathing. Hit a stumbling-block during an important task (like, say, writing a column)? The hand reaches for the phone and opens the social network of choice. A blur of time passes, and half an hour or more of what ought to have been productive effort is gone. A feeling of regret is quickly displaced by the urge to see what has happened on Twitter in the past 15 seconds. Some time after the deadline, the editor asks when exactly to expect the promised copy. Distraction is a constant these days; supplying it is the business model of some of the world’s most powerful firms. As economists search for explanations for sagging productivity, some are asking whether the inability to focus for longer than a minute is to blame.

{kind=link}

As WTO members meet in Argentina, the organisation is in trouble

{kind=link}

“EVERYBODY meets in Buenos Aires,” said Cecilia Malmstrom, the European Union’s trade commissioner, days before heading there for the World Trade Organisation’s (WTO) biennial gathering of ministers, which opens on December 10th. Some non-governmental organisations have been blocked by the protest-averse Argentine authorities, but a meeting of people will indeed take place. One of minds is another matter.

Most participants can agree on one thing. The WTO, which codifies the multilateral rules-based trading system, needs help. President Donald Trump has railed against it and threatened to pull America out. Without American leadership, there is little hope of reaching new deals. And even as the WTO’s dealmaking arm is paralysed, the Trump administration is weakening its judicial one by starving it of judges.

Despite Mr Trump’s threats, America does not seem on the verge of crashing out of a system it helped to construct, to rely entirely on bilateral trade deals and remedies. He...

Marijuana businesses, excluded from finance, are forced to use cash

MANY marijuana growers in northern California, America’s biggest source of the stuff, had expected this autumn’s harvest to be the largest ever. After all, recreational marijuana becomes legal in the state in January. Instead, wildfires in October—spreading so fast they killed 43 people—burned up half the marijuana growing in the area’s tri-county “Emerald Triangle” alone and new fires now raging will claim more. Some reckon the fires set a record not just for burnt pot, but also for the value of banknotes turned to ash.

{kind=link}

Although 29 American states allow sales of marijuana for medical use (or medical and recreational use), federal law still classifies it as a “schedule 1” drug like heroin. Firms handling marijuana proceeds can be prosecuted for money-laundering. Ned Fussell of CannaCraft, a maker of marijuana products, says that a few firms open a bank account under an alternative identity. But banks almost always find out. So cannabis businesses operate almost exclusively in cash. Many...

The euro zone’s boom masks problems that will return to haunt it

“WHAT does not kill me makes me stronger,” wrote Nietzsche in “Götzen-Dämmerung”, or “Twilight of the Idols”. Alternatively, it leaves the body dangerously weakened, as did the illnesses that plagued the German philosopher all his life. The euro area survived a hellish decade, and is now enjoying an unlikely boom. The OECD, a club of mostly rich countries, reckons that the euro zone will have grown faster in 2017 than America, Britain or Japan. But, sadly, although the currency bloc has undoubtedly proven more resilient than many economists expected, it is only a little better equipped to survive its next recession than it was the previous one.

Europe’s crisis was brutal. Euro-area GDP is roughly €1.4trn ($1.7trn)—an Italy, give or take—below the level it would have reached had it grown at 2% per year since 2007. Parts of the periphery have yet to regain the output levels they enjoyed a decade ago (see chart). The damage was exacerbated by deep flaws within Europe’s monetary union. Three shortcomings loomed particularly large. First, the union centralised money-creation but left national governments responsible for their own fiscal solvency. So markets came to understand that governments could no longer bail themselves out by printing money to pay off creditors. The risk of default made markets panic in response to bad news, pushing up government borrowing costs and...

Europe’s banks face a glut of new rules

{kind=link}

FOR those oddballs whose hearts sing at the thought of bank regulation, Europe is a pretty good place to be. No fewer than five lots of rules are about to come into force, are near completion or are due for overhaul. They will open up European banking to more competition, tighten rules on trading, dent reported profits and boost capital requirements. Although they should also make Europe’s financial system healthier, bankers—after a decade of ever-tightening regulation since the crisis of 2007-08—may be less enthused.

Start with the extra competition. On January 13th the European Union’s updated Payment Services Directive, PSD2, takes effect. It sets terms of engagement between banks, which have had a monopoly on customers’ account data and a tight grip on payments, and others—financial-technology companies and rival banks—that are already muscling in. Payment providers allow people to pay merchants by direct transfer from their bank accounts. Account aggregators pull together data...

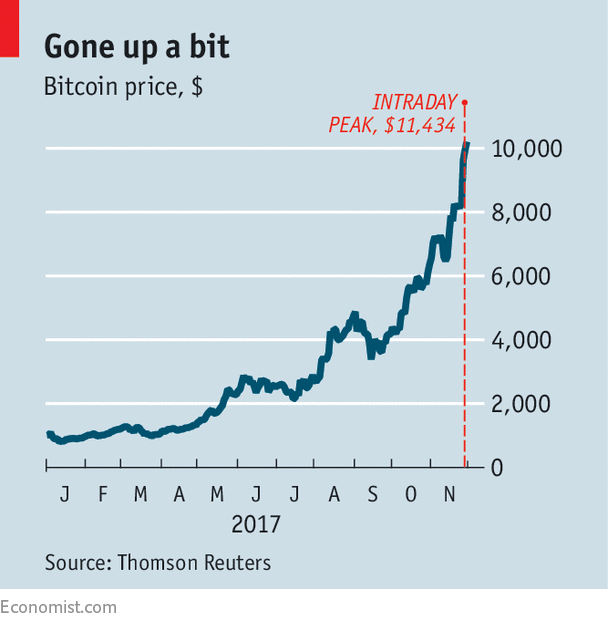

As bitcoin’s price passes $10,000, its rise seems unstoppable

{kind=link}

MOST money these days is electronic—a series of ones and zeros on a computer. So it is rather neat that bitcoin, a privately created electronic currency, has lurched from $1,000 to above $10,000 this year (see chart), an epic journey to add an extra zero.

On the way, the currency has been controversial. Jamie Dimon, the boss of JPMorgan Chase, has called it a fraud. Nouriel Roubini, an economist, plumped for “gigantic speculative bubble”. Ordinary investors are being tempted into bitcoin by its rapid rise—a phenomenon dubbed FOMO (fear of missing out). Both the Chicago Mercantile Exchange, America’s largest futures market, and the NASDAQ stock exchange have seemingly added their imprimaturs by planning to offer bitcoin-futures contracts.

It is easy to muddle two separate issues. One is whether the “blockchain” technology that underpins bitcoin becomes more widely adopted. Blockchains, distributed ledgers that record transactions securely, may prove very useful in some...

A regulatory tempest lashes China’s markets

IT IS is the kind of company that for years was a safe bet for investors. China City Construction is big, government-owned and focused on building basic infrastructure such as sewers. But the bet, it turns out, was not so safe after all. In November China City missed interest payments on three separate bonds, after failing to refinance its hefty debts. It is one of a growing number of victims of the government’s clean-up of the financial system, or what is known in China as the “regulatory storm”.

The storm has been gathering strength for the better part of a year but its intensity over the past couple of weeks has caught many off-guard. The government wasted little time after an important Communist party meeting in October before taking on some of the riskier parts of the financial system. As a result, China’s risk-free interest rate—ie, the yield on government bonds— has shot up. Overall, it has risen by a percentage point since the start of 2017.

For firms, even those closely tied to the state, the rise in borrowing costs has been even steeper. The yield on ten-year bonds issued by China Development Bank, a “policy bank” that finances state projects at home and abroad, has soared to nearly 5%, the highest in three years (see chart).

...

Brazil puts its state development bank on a diet

{kind=link}

IN 2009, as Brazil was buffeted by the global financial crisis, its president, Luiz Inácio Lula da Silva, was seething. The mess, he complained, was the fault of “blue-eyed white people, who previously seemed to know everything, and now demonstrate they know nothing at all”. For him the crisis was a repudiation of Anglo-Saxon liberalism and a vindication of state capitalism. Like many countries, Brazil cut interest rates and increased spending. Unlike many other governments, however, Brazil’s used its state development bank, BNDES, to funnel subsidised credit to Brazil’s largest companies. Thanks to cheap loans from the Treasury, the bank doubled its lending, which reached a peak of 4.3% of GDP in 2010. For most loans the interest rates were half the level of Selic, the central bank’s benchmark.

The plan worked, for a while. Brazil emerged from the crisis relatively unscathed: after a short recession in 2009 the economy rebounded...

India’s new bankruptcy code takes aim at delinquent tycoons

{kind=link}

A SMOOTH bankruptcy process is akin to reincarnation: a company at death’s door gets to shuffle off its old debts, often gain new owners, and start a new life. Might the idea catch on in India? A first wave of cadaverous firms are seeking rebirth under a bankruptcy code adopted in December 2016. In a hopeful development, tycoons once able to hold on to “their” businesses even as banks got stiffed seem likely to be forced to cede control.

India badly needs a fresh approach to insolvent businesses. Its banks’ balance-sheets sag under 8.4trn rupees ($130bn) of loans that will probably not be repaid—over 10% of their outstanding loans. But foreclosure is fiddly: it currently takes over four years to process an insolvency, and recovery rates are a lousy 26%. Partly as a result, bankers have often turned a blind eye to firms they ought to have foreclosed on.

This is bad for the banks and worse for the economy, which has slowed markedly, in part as credit to companies has dried up. The problem festered for years, not...

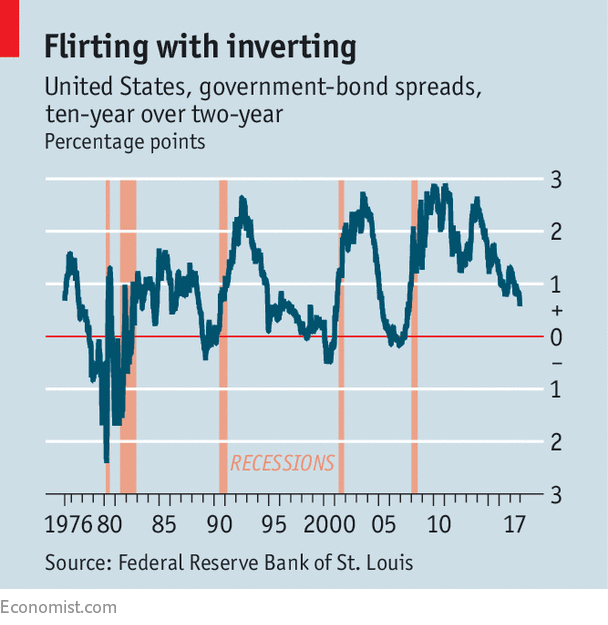

A flattening yield curve argues against higher interest rates

CENTRAL bankers may control short-term interest rates, but long-term ones are mostly free to wander. They do not always behave. When Alan Greenspan, then chairman of the Federal Reserve, was raising short rates in 2005, he described a simultaneous decline in long rates as a “conundrum”. His successor-to-be, Ben Bernanke, blamed foreign investments in American assets because of a “global saving glut”.

Janet Yellen, today’s (outgoing) Fed chair, faces a similar puzzle. Ms Yellen’s Fed has raised rates twice this year, and will probably make it three times in December. In October the Fed began to reverse quantitative easing (QE), purchases of financial assets with newly created money. Despite all this monetary tightening, yields on ten-year Treasury bonds have fallen from around 2.5% at the start of 2017 to about 2.3% today. As a result, the “yield curve” is flattening. The difference between ten-year and two-year interest rates is at its lowest since November 2007 (see chart).

{kind=link}

The...

What cheese can tell you about international barriers to trade

{kind=link}

BEN SKAILES, a British cheesemaker, is busy as Christmas ripens demand for his Stilton. Foreigners make up a third of demand for his dairy, Cropwell Bishop Creamery. This exporting achievement is not to be sniffed at when one considers the barriers to the cheese trade.

Some are natural. Perishable food goes better with wine than long journeys. At least Mr Skailes’s Stilton can survive the three-week trip to America. (His is best eaten within 16 weeks.) Softer cheeses struggle, giving American producers an advantage.

Other hurdles are man-made. Tariffs and quotas are supposed to support domestic dairy industries, and are more onerous than in other sectors. The European Union protects its dairy industry with a 34% average duty, compared with an overall average of 5%. In America it is 17%, compared with 3.5%. Stilton escapes American quotas, but full “loaves” are taxed at a 12.8% rate, or 17% if they arrive sliced. (Unprocessed...

A purge of Russia’s banks is not finished yet

{kind=link}

WHEN Elvira Nabiullina took over the governorship of the Russian Central Bank (CBR) in 2013, she faced a bloated and leaky finance sector with over 900 banks. Since then, more than 340 have lost their licences. Another 35 have been rescued, including, in recent months, Otkritie, once the country’s biggest private lender by assets, and B&N Bank, its 12th largest. The costs have been steep. According to Fitch, a ratings agency, over 2.7trn roubles ($46bn, some 3.2% of GDP in 2016) have been spent on loans to rescued banks and payments to insured depositors. Fitch reckons another few hundred banks could go before the clean-up concludes. More large private banks are whispered to be among them.

The CBR has rightly been praised for preventing a wider crisis and undertaking a clean-up during a punishing recession. Non-performing loans are at a manageable level, of around 10%. Bringing Otkritie and B&N under CBR stewardship calmed panicked markets. Yet nationalisation also raises...

Italy’s new savings accounts fuel a boom in stockmarket listings

ITALY seems an unlikely place to be enjoying a boom in new listings on the stockmarket. It is full of family-run small and medium-sized enterprises (SMEs) that mostly rely for their finance on banks; and Italy’s banks are notorious for the bad debts still lingering on their balance-sheets. But Borsa Italiana, Milan’s stock exchange, has already seen 33 share issues so far this year, of which 24 have been full-fledged initial public offerings (IPOs). The number of listings so far already equals that seen in previous boom years in 2007 or 2015. With more expected before January, the exchange is likely to achieve the highest number of listings since the height of the dotcom bubble in 2000 (see chart).

{kind=link}

A big reason for the surge is the Italian government’s roll-out in February of new individual savings accounts, known as PIRs, which offer favourable tax treatment. These have done better than expected. Asset managers have amassed €7.5bn ($8.3bn) in new PIR funds in the first three quarters of...

The craze for ethical investment has reached Japan

{kind=link}

JAPAN is prone to fads—usually in fancy desserts or fashion ripe for Instagram. A less photogenic one has hit finance: investing in assets screened for ESG (environmental, social and governance) factors. In 2014-16 funds invested in ESG assets grew faster in Japan than anywhere else (and not just because of better reporting and a low base).

Today Japan’s sustainable-investment balance is $474bn, or some 3.4% of the country’s total managed assets—low compared with Europe or America, but high for Asia. The shift is driven from the top down, rather than, as elsewhere, by ethically minded individual investors.

When he returned to power in 2012 with a plan to revitalise the economy Shinzo Abe, Japan’s prime minister, wanted to reform Japan’s conservative business culture. A code for institutional investors was introduced in 2014, followed by one on corporate governance a year later. The government’s aim is not only to get firms to distribute some of their vast piles of...

Ethical investors set their sights on index funds

{kind=link}

VANGUARD, an American fund-management giant, promises “the highest standards of ethical behaviour”. Its low fees, helpful call centres and lack of scandal give the claim credence. It is by far the largest mutual-fund group, with $4.8trn under management. It receives more than half of all the new money going into American mutual funds. Most ends up in its passively managed offerings that track indices.

So you might think its shareholder meetings would be pious celebrations. Instead, Vanguard tries to avoid them. On November 15th it held its first since 2009, to satisfy a legal requirement that two-thirds of fund directors are elected rather than appointed. It held the meeting near its Arizona satellite office, far from its Philadelphia-area headquarters. Only 200 of its 20m clients showed up, trudging through metal detectors and tight security.

Vanguard may have been pleased by the small turnout. Among those dogged 200 who attended were representatives of an...

- « primera

- ‹ anterior

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- siguiente ›

- última »