The Economist - Finance and economics

The Paradise Papers shed new light on offshore finance

{kind=link}

THIS week was uncomfortable for a host of well-heeled figures. In the frame were U2’s Bono, America’s commerce secretary, Wilbur Ross, and Britain’s Queen Elizabeth, as well as some of the world’s most valuable companies, including Apple and Nike. All these, and many more, feature in the “Paradise Papers”, a trove of more than 13m documents, many of them stolen from Appleby, a leading offshore law firm. The International Consortium of Investigative Journalists (ICIJ) and its 95 press partners, including the BBC and the New York Times, began publishing stories based on the papers on November 5th. Dozens appeared this week, with more to follow after The Economist went to press.

The ICIJ’s last big splash, the Panama Papers in April 2016, shed light on some of the darkest corners of offshore finance. In contrast, many of the activities highlighted by this leak are legal. But they would be widely seen as flouting the spirit of national tax laws by exploiting the gaps that open up...

Equity valuations are high. But other options look even worse

{kind=link}

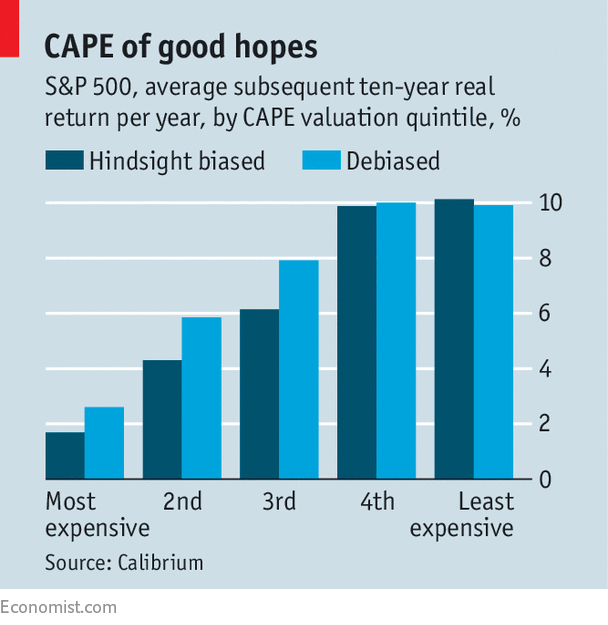

EVERY investor would like to find the perfect measurement tool to tell them when to get into, and out of, the stockmarket. The cyclically adjusted price-earnings ratio (CAPE), as calculated by Robert Shiller of Yale University, averages profits over ten years and is used by many as an important valuation indicator. Currently it shows that American shares have hitherto been more highly valued only in 1929 and the late 1990s, periods that were followed by big crashes.

That seems ominous. But as a paper by Dylan Grice and Gregor Obrecht of Calibrium, a Zurich-based private-investment office, makes clear, it is far from conclusive. The CAPE is not much use as a short-term indicator; it has been well above its long-term average for several years now, as it was in the late 1990s.

The main argument for the CAPE is a long-term one. If you divide all past CAPE values into quintiles, the annual returns earned over the subsequent decade by investing in equities when the CAPE was in...

Venezuela seeks the restructuring of its massive foreign debts

Maduro has a cunning plan. Maybe

{kind=link}

INVESTORS have long seen a default on Venezuelan sovereign debt as a question of when, not if. Its bonds have been priced at levels implying imminent bankruptcy, but somehow the cash-strapped oil exporter has stayed afloat. Until now. On November 2nd Nicolás Maduro, the country’s authoritarian president, announced that he would order a “refinancing and restructuring” of foreign debt worth about $105bn. The prices of government bonds fell by up to half. Markets braced themselves for one of history’s most complex sovereign-debt renegotiations.

Mr Maduro’s brief statement was cryptic as to the concrete steps he will take. He invited “everyone involved in foreign debt” to talks in Caracas, the capital, on November 13th. Many creditors want a neutral venue. Moreover, Mr Maduro appears to have pre-emptively dashed any hope of a voluntary agreement by naming his vice-president, Tareck El Aissami, as head of his debt-restructuring committee. America’s Treasury department...

What there is to learn from the Soviet economic model

{kind=link}

IN 1955 Jawaharlal Nehru, the prime minister of India, embarked on a 16-day tour of the Soviet Union. He was like a “kid in a candy store”, according to one editor of his letters. Besides the Bolshoi ballet and the embalmed corpse of Stalin, he visited a Stalingrad tractor works, a machinery-maker in Yekaterinburg and an iron-and-steel plant in Magnitogorsk. In a letter, he wondered if the Soviet Union’s economic approach, “shorn of violence and coercion”, could help the world achieve peace and prosperity.

The answer, of course, was “no”. But Nehru concluded otherwise, incorporating Soviet ideas into India’s five-year plans and welcoming Soviet aid, equipment and expertise. In the year of his visit, the Russians set up a steel factory in what is now the Indian state of Chhattisgarh. It became India’s main supplier of rails.

Nehru was not alone. The Soviet model impressed many leaders in the poorer parts of the world. Even today, according to Charles Robertson of...

The New York Fed’s president announces his retirement

He never really took the bull by the horns

{kind=link}

APPLICATIONS sought for leading Wall Street post. Duties: important role in setting interest rates (some vaguely defined other responsibilities). Perks: lovely office in Italianate palace; large staff. Requirements: eligibility for highest-level security clearance; tacit support in Washington, DC. Desirable but optional: broad knowledge of banking.

This week the New York Federal Reserve Bank announced that its president, Bill Dudley, will retire next year. He will leave a mixed legacy. He is thought to have given important help to Janet Yellen, the outgoing chair of the Federal Reserve. But he also presided over a steep decline in his institution’s influence over the banks that used to revere and fear it.

Located in America’s financial centre, the New York Fed has powers not vested in the country’s 11 other reserve banks. Its president has a permanent seat on the Fed committee that sets interest rates. Its trading desk puts board policies into...

In Japan, the move from cash to plastic goes slowly

{kind=link}

BIC CAMERA, a Japanese electronics retailer, accepts payments in so many ways that the list nearly obscures the till: credit, debit and pre-paid cards; mobile wallets; ApplePay and Alipay; and, in some stores since April, bitcoin too.

Efforts are under way to wean Japan off genkin, or cash. Handling notes and coins is expensive for businesses; many operate on tight margins because a persistent lack of inflation has inhibited price rises. The government reckons more cashless payments could help the economy, too, encouraging people, including a growing number of tourists, to spend more. (And help it collect more tax.) Entrepreneurs think the data that come with cashless methods could promote new business.

Yet cash still dominates. Thank a preponderance of ATMs in ubiquitous konbini (convenience stores), safe cities where people are happy to carry wads of cash, and wariness about handing over personal data. Last year cash accounted for 62% of consumer transactions by...

Jerome Powell is poised to be named chairman of the Fed

{kind=link}

YOU could forgive Janet Yellen, the chair of the Federal Reserve, for feeling peeved. With unemployment at just 4.2%, and inflation at 1.6%, she is close to achieving the Fed’s two goals of curbing joblessness and pinning price rises at 2%. Ms Yellen is a Democrat appointed by Barack Obama in 2014. The tenures of past three Fed chairs were all extended by presidents from the other party. Yet as we went to press, President Donald Trump was expected to nominate Jerome Powell, a Republican on the Fed’s board, to replace Ms Yellen.

If picked, Mr Powell—also an Obama appointee—would stand out from recent incumbents. He would be the first Fed chairman since William Miller, who left office in 1979, with no formal economics training; and, according to the Washington Post, the richest since the 1940s.

Mr Powell, who is 64, is a lawyer-turned-banker. His first role in Washington was at the Treasury during...

Increasingly, hunting money-launderers is automated

{kind=link}

KEEN, no doubt, to stay alive, drug traffickers tend to be prompter payers than most. For software firms, this is just one of many clues that may hint at the laundering of ill-gotten money. Anti-money-laundering (AML) software, as it is called, monitors financial transactions and produces lists of the people most likely to be transferring the proceeds of crime.

Spending on this software is soaring. Celent, a research company, estimates that financial firms have spent roughly $825m on it so far this year, up from $675m last year. Technavio, another research firm, reckons the market is even bigger and will grow at more than 11% annually in coming years. This is partly because authorities are increasingly quick to punish institutions that let down their guard. Deutsche Bank, for example, has been hit with fines worth at least $827m this year alone. Governments, eager to appear tough on crime, are urging prosecutors to go after not just institutions, but also their employees.

...

As the global economy picks up, inflation is oddly quiescent

{kind=link}

A FEW years ago, the news about the euro-zone economy was uniformly bad to the point of tedium. These days, it is the humdrum diet of benign data that prompts a yawn. Figures this week show that GDP rose by 0.6% in the three months to the end of September (an annualised rate of 2.4%). The European Commission’s economic-sentiment index rose to its highest level in almost 17 years. Yet when the European Central Bank’s governing council gathered on October 26th, it decided to keep interest rates unchanged, at close to zero, and to extend its bond-buying programme (known as quantitative easing, or QE) for a further nine months.

The central bank said it would slow down the pace of bond purchases each month, to €30bn ($35bn) from January. But Mario Draghi, the bank’s boss, declined to set an end-date for QE. A hefty dose of easy money will be necessary, he argued, until inflation durably converges on the ECB’s target of just below 2%. It shows few signs of doing so, despite the economy’s...

October 30th marked the 70th birthday of the WTO’s precursor

{kind=link}

SUPERLATIVES surrounded the General Agreement on Tariffs and Trade (GATT) when it was signed on October 30th 1947. A press release heralded it as “the most far-reaching negotiation[s] ever undertaken in the history of world trade.” The Economist grumbled it was “one of the longest and most complicated public documents ever issued—and one of the hardest to comprehend.” The Daily Express, a British newspaper, growled: “The big bad bargain is sealed.”

The agreement’s complexity matched the tangle of global trade affairs. In the preceding decades a thicket of protectionism had strangled commerce and slowed recovery from the Depression of the 1930s. The GATT’s length matched its scope. It included both tariff cuts and promises to forswear new duties. Covering 23 countries responsible for 70% of world trade, it came to embody the rules-based multilateral system.

After 48 years as a...

Asian households binge on debt

{kind=link}

ONE of the more persistent beliefs about the global economy is that Asians are more frugal than others. Explanations have drawn on culture (the self-discipline of Confucianism), history (memories of privation) and public policy (flimsy social safety-nets forcing people to save). For Lee Kuan Yew, the founding father of Singapore, and other theorists of “Asian values”, thrift was one of them. Whatever the true reason, data long supported the basic claim that Asian households were indeed careful with their cash. But over the past few years consumers across the region have done their best to prove that prudence was perhaps just a passing phase.

Household debt in advanced economies has generally declined as a percentage of GDP since the 2008 global financial crisis, according to the Bank for International Settlements. In a number of Asian countries, however, it has been going in the opposite direction (see chart). The biggest increase has been in China, where households have borrowed about $4.5trn over the past decade. But Chinese...

Catalonia and the perils of fiscal redistribution

{kind=link}

POPULISM is the weapon not just of the downtrodden. As the crisis in Catalonia demonstrates, the rich have economic anxieties of their own. Catalonia has an identity distinct, in important ways, from that of the rest of Spain. But the recent drive for independence has been energised by anger over the flow of fiscal redistribution from rich Catalans to their countrymen: people seen, in parts of the restless north-east, as thankless and lazy as well as alien. Paradoxically, globalisation has inflamed separatism around the world by raising the question Catalans now confront: to whom, exactly, do we owe a sense of social responsibility?

Every country or restive region has its own idiosyncratic history. Yet over the long run national borders are surprisingly malleable. Some circumstances offer better prospects for the small and newly independent than others. The smaller the country, the more easily its government can satisfy its people’s political preferences. A broadly satisfying...

Investors call the end of the government-bond bull market (again)

{kind=link}

FOR the umpteenth time in the past decade, a great turning-point has been declared in the government-bond market. Bond yields have risen across the world, including in China, where the yield on the ten-year bond has come close to 4% for the first time since 2014. The ten-year Treasury-bond yield, the most important benchmark, has risen from 2.05% in early September to 2.37%, though that is still below its level of early March (see chart).

{kind=link}

Investors have been expecting bond yields to rise for a while. A survey by JPMorgan Chase found that a record 70% of its clients with speculative accounts had “short” positions in Treasury bonds—ie, betting...

Firms should make more information about salaries public

{kind=link}

SWEDES discuss their incomes with a frankness that would horrify Britons or Americans. They have little reason to be coy; in Sweden you can learn a stranger’s salary simply by ringing the tax authorities and asking. Pay transparency can be a potent weapon against persistent inequities. When hackers published e-mails from executives at Sony Pictures, a film studio, the world learned that some of Hollywood’s most bankable female stars earned less than their male co-stars. The revelation has since helped women in the industry drive harder bargains. Yet outside Nordic countries transparency faces fierce resistance. Donald Trump recently cancelled a rule set by Barack Obama requiring large firms to provide more pay data to anti-discrimination regulators. Even those less temperamentally averse to sunlight than Mr Trump balk at what can seem an intrusion into a private matter. That is a shame. Despite the discomfort that transparency can cause, it would be better to publish more information....

Firms should make more information about salaries public

SWEDES discuss their incomes with a frankness that would horrify Britons or Americans. They have little reason to be coy; in Sweden you can learn a stranger’s salary simply by ringing the tax authorities and asking. Pay transparency can be a potent weapon against persistent inequities. When hackers published e-mails from executives at Sony Pictures, a film studio, the world learned that some of Hollywood’s most bankable female stars earned less than their male co-stars. The revelation has since helped women in the industry drive harder bargains. Yet outside Nordic countries transparency faces fierce resistance. Donald Trump recently cancelled a rule set by Barack Obama requiring large firms to provide more pay data to anti-discrimination regulators. Even those less temperamentally averse to sunlight than Mr Trump balk at what can seem an intrusion into a private matter. That is a shame. Despite the discomfort that transparency can cause, it would be better to publish more information....

Italy’s fourth-biggest bank returns to the stockmarket

{kind=link}

A TELEVISION advertisement for Monte dei Paschi di Siena begins with a toddler tumbling and a gymnast stumbling. “Falling is the first thing we learn,” declares the voice-over. “The second is getting up again.” Italy’s fourth-biggest bank and the world’s oldest, which was bailed out by the Italian government in July, has had several bruising falls over the years. On October 25th it returned to the stockmarket after a ten-month hiatus—the latest stage of its plan to get back on its feet. The shares closed higher on the day, at €4.55 ($5.37), but still far below the €6.49 the government paid.

Trading was suspended last December, after a failed private-sector attempt to save the bank through a share issue. The government said it would get involved. In July the European Commission approved a €8.1bn “precautionary recapitalisation”. European rules say banks receiving such aid must be solvent, the capital injection must not distort competition and the capital shortfall must be...

India recapitalises its state-owned banks

{kind=link}

ONE of the perks of owning a bank is the ability to tap it when you need money. The Indian government, which has majority stakes in 21 lenders, is no exception. As it happens, it needs to finance a bail-out of the banks it owns, most of which are in trouble. So under a cunning plan unveiled on October 24th, the ailing banks will lend the government 1.35trn rupees ($21bn), about a third of their combined market value. The government will reinvest this money in bank shares, thus ensuring they no longer need a bail-out.

Steadying a tottering financial system is never a graceful exercise, as American and European authorities discovered after the financial crisis. India’s lenders withstood the meltdown of 2007-08 well, but then embarked on an ill-advised lending spree, backing lots of infrastructure projects that got snarled in bureaucracy. Bad loans piled up. State-owned lenders, which account for around two-thirds of the sector, now...

Millennials are doing better than the baby-boomers did at their age

ALL men are created equal, but they do not stay that way for long. That is one message of a report this month by the OECD, a club of 35 mostly rich democracies. Many studies show how income gaps have evolved over time or between countries. The OECD’s report looks instead at how inequality evolves with age.

As people build their careers, or don’t, their incomes tend to diverge. This inequality peaks when a generation reaches its late 50s. But it tends to fall thereafter, as people draw redistributive public pensions and quit the rat race, a contest that tends to give more unto every one that hath. Old age, the OECD notes, is a “leveller”.

Will it remain so? Retirement, after all, flattens incomes not by redistributing from rich seniors to poor, but by transferring money to old people from younger, working taxpayers. There will be fewer of them around in the future for every retired person, reducing the role of redistributive public pensions.

One logical response to the diminishing number of workers per pensioner is to raise the retirement age. But that will exacerbate old-age inequality, if mildly. Longer careers will give richer workers more time to compound their advantages. And when retirement eventually arrives, the poor, who die earlier, will have less time to enjoy their pensions.

Today’s youngsters may resent having to provide for...

Silicon speculators

{kind=link}

EXCHANGE-TRADED funds (ETFs) were supposed to make investing easy. Instead of spending hours researching individual stocks and bonds or paying an expert fund manager, investors could simply buy a few ETFs. But now there are too many to choose from. BlackRock offers 346 in America alone. Some investors need help allocating their money between different funds. Many companies now offer “automated wealth managers” (AWMs) that perform this service.

AWMs have been around for less than ten years, but they have proliferated, offering different services in different countries. Often, they are called “robo-advisers”, but this term can be misleading. Some offer clients detailed advice about how to save. For example, Wealthfront, an American AWM, predicts the cost of sending a student to a given college, taking into account increases in tuition fees and likely financial aid. It then suggests how parents can save in a tax-efficient way. Other...

Will corporate tax cuts boost workers’ wages?

THE president’s tax promise has always been clear: he will reduce the amount middle-earners, but not rich Americans, must pay. Yet every time Donald Trump releases a plan, analysts say it does almost the opposite. The Tax Policy Centre, a think-tank, recently filled in the blanks in the latest Republican tax proposals and concluded that more than half of its giveaways would go to the top 1% of earners. Their incomes would rise by an average of $130,000; middle-earners would get just $660. The White House maintains that tax reform will deliver a much heftier boost to workers’ pay packets. Who is right?

The disagreement boils down to who benefits when taxes on corporations fall. The Tax Policy Centre says it is mainly rich investors. But in a report released on October 16th, Mr Trump’s Council of Economic Advisers (CEA) claimed that cutting the corporate-tax rate from 35% to 20%, as Republicans propose, would eventually boost annual wages by a staggering $4,000-9,000 for the average household.

The claim has sparked a debate among economists that is as ill-tempered as it is geeky. Left-leaning economists are incredulous. Writing in the Wall Street Journal, Jason Furman, who led the CEA under Barack Obama, pointed out that if the report is right, wage increases would total about three to six times the cost of the tax cut. Larry...

- « primera

- ‹ anterior

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- siguiente ›

- última »