Agregador de fuentes

Trilobites: You Won’t Like This News About Bedbugs, Ticks and the ‘Bomb Cyclone’

That Recent Brutally Cold Weather? It’s Getting Rarer

Once an ISIS Recruiter, She Now Wants Out

Six New Cocktails, Alcohol Not Included

Texas Illegally Excluded Thousands From Special Education, Federal Officials Say

Moira Donegan Says She Created List of Men in Media Accused of Misconduct

Book Entry: Review: Even on the Internet, What’s Old Is New Again

Review: With ‘False Flag,’ Israel Exports Another Fine Thriller

The Analytics Guy Failed to Compute One Thing: How to Be Accepted in Mexico

A Greener, More Healthful Place to Work

Matter: Climate Change Is Altering Lakes and Streams, Study Suggests

Frugal Traveler: Ways to Save in 2018

Can a ‘No Excuses’ Charter Teach Students to Think for Themselves?

The Carpetbagger: Oscars So Awkward? Trying to Top the Globes Won’t Be Easy

Front and Center: Celebrating Black Comics and Their Creators

‘Dreamers,’ 7-Eleven, Michelle Williams: Your Thursday Briefing

How China won the battle of the yuan

“THE horse may be out of the proverbial barn.” So wrote Ben Bernanke, a former chairman of the Federal Reserve, in early 2016, arguing that capital controls might be powerless to save China from a run on its currency. He was far from alone at the time. As cash rushed out of the country, analysts debated whether the yuan would collapse, and some hedge funds bet that day was coming fast. But two years on, the horse is back in the barn: the government’s defence of the yuan has succeeded, in part through tighter capital controls.

The latest evidence was an 11th consecutive monthly increase in foreign-exchange reserves in December. During that time China’s stockpile of official reserves, the world’s biggest, climbed by $142bn, reaching $3.14trn, roughly double the cushion usually regarded as needed to ensure financial stability. Another sign of China’s success is the yuan itself. At the start of 2017 the consensus of forecasters was that the currency would continue to weaken; it finished the year up by 6% against the dollar.

Investors and analysts were not wrong in viewing Chinese capital controls as porous. Enterprising types had—and have—umpteen ways to sneak money out, from overpaying for imports to smuggling cash across the border in luggage. But there is a wide spectrum between a fully open and fully closed capital account, and China has showed over...

Accountancy takes root in the inhospitable soil of Afghanistan

{kind=link}

WHEN Afghan lawmakers were debating rules of conduct for accountants, some were confounded by their strictness. Why should those found guilty of murder, asked one member of parliament, be struck off? That is a sign of the challenges facing the professional body for bean-counters, Certified Professional Accountants (CPA) Afghanistan, which was launched last month.

Attempts to establish a home-grown profession start from a low base. Back in 2009 Kabul, a city of around 4m, had fewer than 20 qualified accountants. Neither standards nor oversight for the profession were in place. Most local outfits were branches of firms from elsewhere in South Asia or farther afield.

Boring old accountancy might not seem a priority for a war-torn country. But in business it can foster trust and transparency—scarce commodities in a country where corruption is systemic. Because of the difficulty of verifying borrowers’ financial positions and...

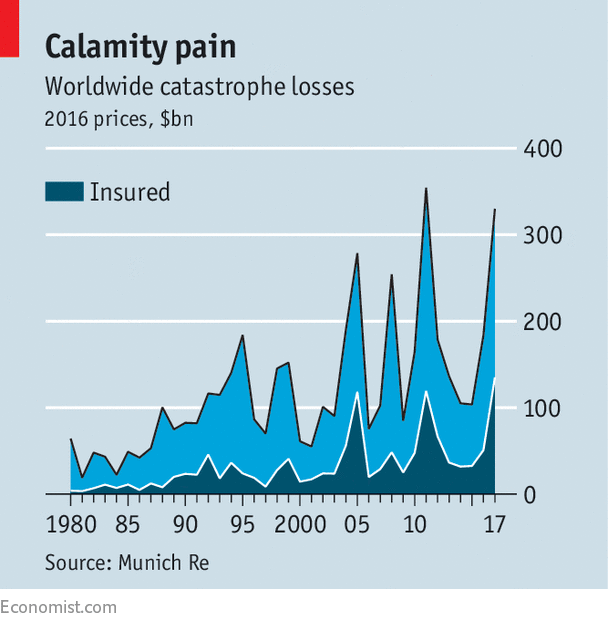

Natural disasters made 2017 a year of record insurance losses

THAT 2017 suffered from more than its fair share of natural catastrophes was known at the time. In the wake of Hurricane Harvey, the streets of Houston, Texas, were submerged under brown floodwater; Hurricane Irma razed buildings to the ground on some Caribbean islands. That the destruction was great enough for insurance losses to reach record levels has only just been confirmed. According to figures released on January 4th by Munich Re, a reinsurer, global, inflation-adjusted insured catastrophe losses reached an all-time high of $135bn in 2017 (see chart). Total losses (including uninsured ones) reached $330bn, second only to losses of $354bn in 2011.

{kind=link}

A large portion of the losses in 2011 was caused by one catastrophe: the earthquake and tsunami in Japan. Losses in 2017 were largely traceable to extreme weather. Fully 97% were weather-related, well above the average since 1980 of 85%. If climate change brings more frequent extreme weather, as Munich Re and others expect, last year’s loss levels...

Donald Trump’s difficult decision on steel imports

{kind=link}

EVERY Tuesday, senior members of the administration gather in the White House to discuss trade. They are divided between hawks, who argue that America needs to be tougher in its defence against what they see as economic warfare waged by China, and doves, who worry about the costs of conflict. So far, against all expectations when President Donald Trump entered the White House, the doves have prevailed. The first of a series of legal deadlines could soon unleash the hawks.

Last April Wilbur Ross, the commerce secretary, initiated a probe into whether steel imports were a threat to America’s national security. His department pointed to a “dramatic” increase in steel imports over the previous year and to the idling of nearly 30% of America’s steel-production capacity, as imports feed a quarter of its consumption. If the report, due by January 15th, finds imports are a threat, Mr Trump, under Section 232 of the Trade Expansion Act of 1962, will have 90 days to respond.

The report’s...