Agregador de fuentes

Take a Number: Women Are More Likely to Address High Blood Pressure

Economic View: A Stock Market Panic Like 1987 Could Happen Again

Contributing Op-Ed Writer: Democracy Can Plant the Seeds of Its Own Destruction

California Today: California Today: Why Jerry Brown Vetoes

Review: ‘Wonderstruck,’ Todd Haynes’s Imitations of Life

Review: Colin Farrell, Nicole Kidman and ‘The Killing of a Sacred Deer’

A Madoff Gets a Makeover, by Giving Them

How should recessions be fought when interest rates are low?

{kind=link}

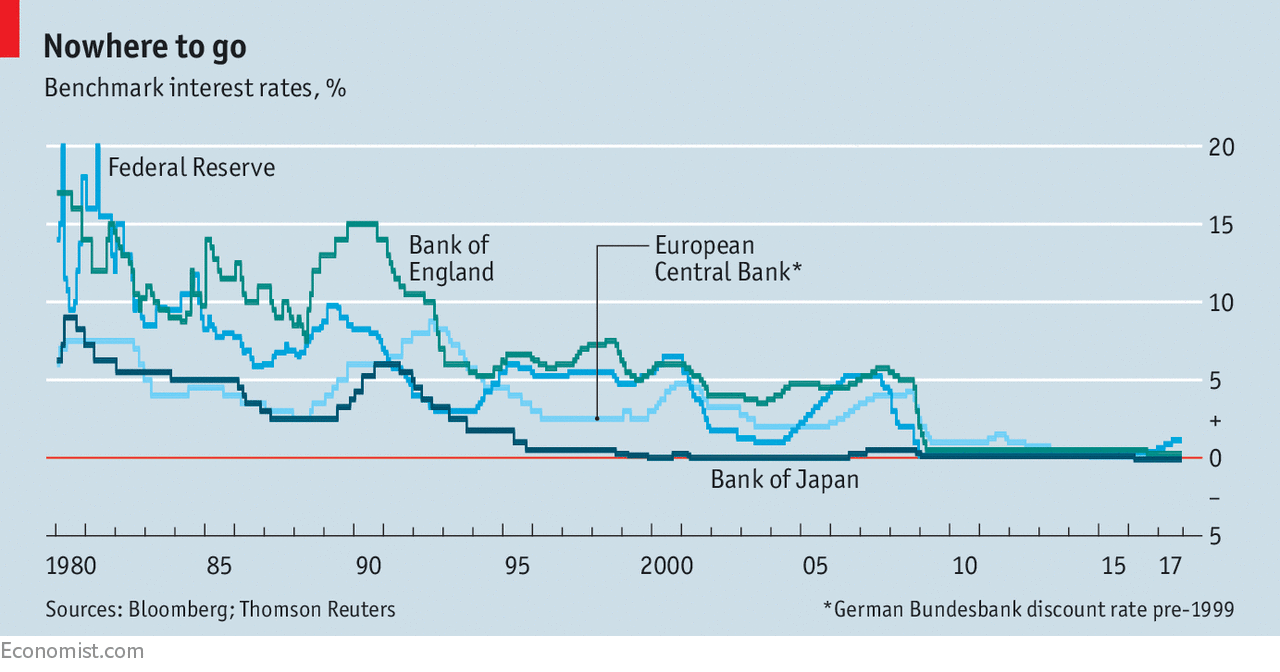

ONE day, perhaps quite soon, it will happen. Some gale of bad news will blow in: an oil-price spike, a market panic or a generalised formless dread. Governments will spot the danger too late. A new recession will begin. Once, the response would have been clear: central banks should swing into action, cutting interest rates to boost borrowing and investment. But during the financial crisis, and after four decades of falling interest rates and inflation, the inevitable occurred (see chart). The rates so deftly wielded by central banks hit zero, leaving policymakers grasping at untested alternatives. Ten years on, despite exhaustive debate, economists cannot agree on how to handle such a world.

{kind=link}

Higher taxes can lower inequality without denting economic growth

{kind=link}

INEQUALITY is one of the big political issues of the 21st century, with many commentators citing it as a significant factor behind the rise of populism. After all, nothing could be more indicative of the triumph of the common man than the elevation of a property billionaire to the American presidency.

A new IMF report* looks at how fiscal policy can help tackle inequality. In advanced economies, taxation already has an impact. The Gini coefficient (a standard measure of income inequality) is around a third lower after taxes and transfers than it is before them. But whereas such policies offset around 60% of the change in market inequality between 1985 and 1995, they have had barely any impact since.

That is because of a change in policy direction. Across the West, taxes on higher incomes have generally fallen. This could be for a number of reasons, the IMF says. The tax take from high earners could have become more “elastic” (ie, sensitive to rate changes); in a mobile...

Politics ensnares South Africa’s biggest asset manager

{kind=link}

THE rot in South African politics, which has eaten away at state companies, is spreading. This week McKinsey, a consultancy, apologised for the “distress” it had caused the South African people. Political mud had already drowned Bell Pottinger, a British public-relations firm, and forced resignations at KPMG, an auditor. So the shenanigans at the government-owned Public Investment Corporation (PIC), have set off alarm bells. One concern is an apparent attempt to oust Dan Matjila, its boss. A linked worry is whether PIC funds will be used to prop up state businesses.

The PIC is a lucrative prize: it is Africa’s largest money manager, controlling 1.9trn rand ($140bn) of assets, mostly the pensions of state employees, and holding 11% of shares in South Africa’s biggest 25 companies. So anonymous allegations against Mr Matjila, including the claim that he had misdirected funds to his girlfriend’s business, naturally provoked a furore. On...

Workers are not switching jobs more often

{kind=link}

EVERYBODY knows—or at least thinks he knows—that a millennial with one job must be after a new one. Today’s youngsters are thought to have little loyalty towards their employers and to be prone to “job-hop”. Millennials (ie, those born after about 1982) are indeed more likely to switch jobs than their older colleagues. But that is more a result of how old they are than of the era they were born in. In America at least, average job tenures have barely changed in recent decades.

Data from America’s Bureau of Labour Statistics show workers aged 25 and over now spend a median of 5.1 years with their employers, slightly more than in 1983 (see chart). Job tenure has declined for the lower end of that age group, but only slightly. Men between the ages of 25 and 34 now spend a median of 2.9 years with each employer, down from 3.2 years in 1983.

...

A rash of bankruptcies hits Chinese lenders backed by state firms

{kind=link}

THE Communist Party dominates China’s economy and uses state-run companies, which it controls with an iron fist, to enforce its diktats. Or so the theory goes. Reality is messier: the party often struggles to monitor state-owned enterprises (SOEs), let alone to get them to toe its line. As it convenes its five-yearly congress, one of the financial system’s dodgiest corners has served up a reminder of the limits to its power.

In the past two months at least seven online lenders backed by SOEs have collapsed. It was a business none should have been in, far removed from the industries they were supposed to focus on. The money potentially lost is trivial—roughly 1bn yuan ($150m), compared with government assets worth more than 100trn yuan. Still, these cases highlight how hard it is for the party to stamp its authority on the vast state sector.

The troubled SOEs include distant subsidiaries of the national nuclear company, an aviation company and a big energy...

A Lloyd’s report urges insurers to ask “what if?”

{kind=link}

ON JULY 7th disaster was narrowly averted when an Air Canada passenger plane, trying to land on a full taxiway at San Francisco airport, pulled up just in time. Five seconds longer, and it might have crashed into fully loaded planes and killed over 500 people, in potentially the deadliest aviation disaster ever. Instead, the incident became a non-event—not just in collective memory but also in insurance. With no losses, there was nothing to log. Yet ignoring such near-misses, argues a report published this week by Lloyd’s of London, an insurance market, and RMS, a risk-modeller, is a missed opportunity.

Counterfactual “what if” thinking may be an enjoyable pastime for historians—“What if Hitler had been assassinated?” being one favourite—but is not common among underwriters. They prefer to base estimates of future risk—and hence premiums—on hard data of what happened in the past, eg, the number of aeroplanes that crashed and the total losses incurred. Since actual aviation losses...

Multilateral lenders vow openness about their carbon footprints

{kind=link}

THE World Bank gets a lot of flak. Developing countries clamour for a bigger role in its management. President Donald Trump’s administration lambasts it for lending too much to China. Last year employees openly griped about a crisis of leadership under their boss, Jim Yong Kim. Now the embattled institution faces criticism from a traditionally friendlier quarter: environmentalists. They accuse it and other multilateral development banks (MDBs) of not being upfront about their true carbon footprint.

That must hurt. After all, MDBs pioneered climate-friendly finance. Ten years ago the European Investment Bank issued the world’s first green bond to bolster renewables and energy-efficiency schemes. The World Bank has not backed a coal-fired plant since 2010. In 2011-16 it and the five big regional lenders in the Americas, Asia, Africa and Europe offered developing countries a total of $158bn to help combat climate change and adapt to its effects. They disclose the amount of...