Agregador de fuentes

Malta, Where the West Was Born

The Enthusiast: In Praise of the ‘Career Romance’

Fact Check: The Senate G.O.P. Tax Plan

The President Who Politicked Oklahoma Back to the Top

The Pour: Five Wine Books to Give This Holiday Season

Donald Trump, Garrison Keillor, Jay-Z: Your Thursday Briefing

Review: ‘The Shape of Water’ Is Altogether Wonderful

Hungry City: Around the Corner, Thai Desserts Await

Best of Late Night: Stephen Colbert Is Appalled by the Allegations Against Matt Lauer

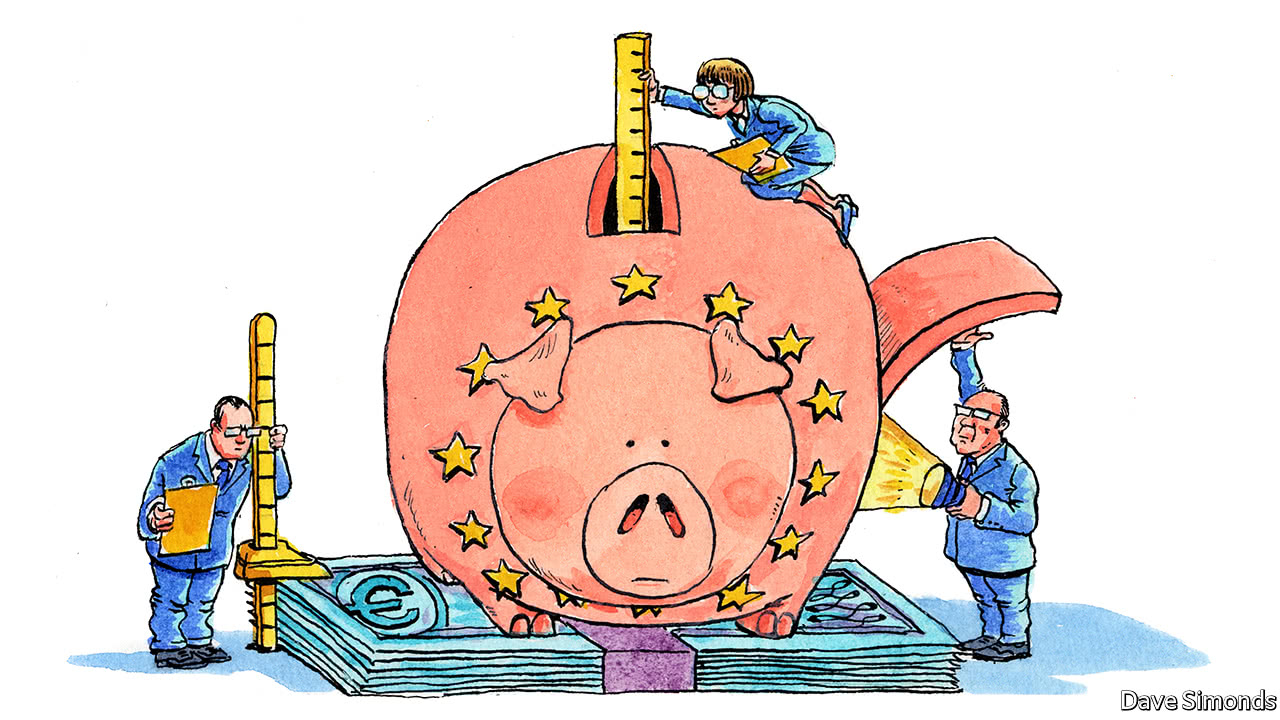

The euro zone’s boom masks problems that will return to haunt it

“WHAT does not kill me makes me stronger,” wrote Nietzsche in “Götzen-Dämmerung”, or “Twilight of the Idols”. Alternatively, it leaves the body dangerously weakened, as did the illnesses that plagued the German philosopher all his life. The euro area survived a hellish decade, and is now enjoying an unlikely boom. The OECD, a club of mostly rich countries, reckons that the euro zone will have grown faster in 2017 than America, Britain or Japan. But, sadly, although the currency bloc has undoubtedly proven more resilient than many economists expected, it is only a little better equipped to survive its next recession than it was the previous one.

Europe’s crisis was brutal. Euro-area GDP is roughly €1.4trn ($1.7trn)—an Italy, give or take—below the level it would have reached had it grown at 2% per year since 2007. Parts of the periphery have yet to regain the output levels they enjoyed a decade ago (see chart). The damage was exacerbated by deep flaws within Europe’s monetary union. Three shortcomings loomed particularly large. First, the union centralised money-creation but left national governments responsible for their own fiscal solvency. So markets came to understand that governments could no longer bail themselves out by printing money to pay off creditors. The risk of default made markets panic in response to bad news, pushing up government borrowing costs and...

Europe’s banks face a glut of new rules

{kind=link}

FOR those oddballs whose hearts sing at the thought of bank regulation, Europe is a pretty good place to be. No fewer than five lots of rules are about to come into force, are near completion or are due for overhaul. They will open up European banking to more competition, tighten rules on trading, dent reported profits and boost capital requirements. Although they should also make Europe’s financial system healthier, bankers—after a decade of ever-tightening regulation since the crisis of 2007-08—may be less enthused.

Start with the extra competition. On January 13th the European Union’s updated Payment Services Directive, PSD2, takes effect. It sets terms of engagement between banks, which have had a monopoly on customers’ account data and a tight grip on payments, and others—financial-technology companies and rival banks—that are already muscling in. Payment providers allow people to pay merchants by direct transfer from their bank accounts. Account aggregators pull together data...

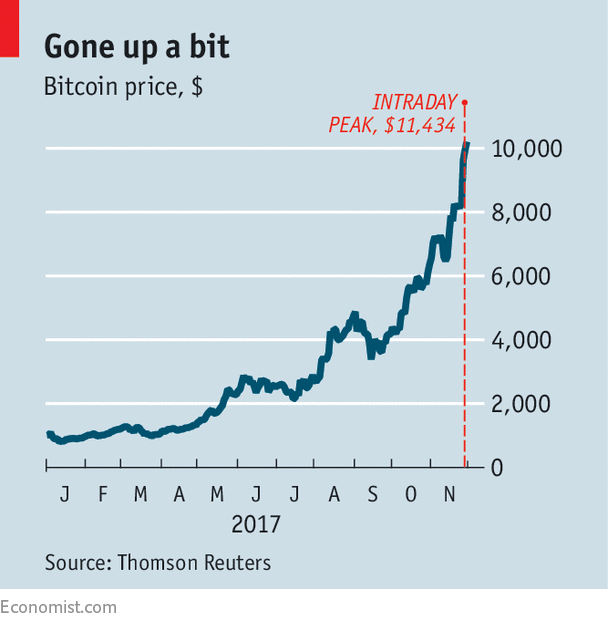

As bitcoin’s price passes $10,000, its rise seems unstoppable

{kind=link}

MOST money these days is electronic—a series of ones and zeros on a computer. So it is rather neat that bitcoin, a privately created electronic currency, has lurched from $1,000 to above $10,000 this year (see chart), an epic journey to add an extra zero.

On the way, the currency has been controversial. Jamie Dimon, the boss of JPMorgan Chase, has called it a fraud. Nouriel Roubini, an economist, plumped for “gigantic speculative bubble”. Ordinary investors are being tempted into bitcoin by its rapid rise—a phenomenon dubbed FOMO (fear of missing out). Both the Chicago Mercantile Exchange, America’s largest futures market, and the NASDAQ stock exchange have seemingly added their imprimaturs by planning to offer bitcoin-futures contracts.

It is easy to muddle two separate issues. One is whether the “blockchain” technology that underpins bitcoin becomes more widely adopted. Blockchains, distributed ledgers that record transactions securely, may prove very useful in some...

A regulatory tempest lashes China’s markets

IT IS is the kind of company that for years was a safe bet for investors. China City Construction is big, government-owned and focused on building basic infrastructure such as sewers. But the bet, it turns out, was not so safe after all. In November China City missed interest payments on three separate bonds, after failing to refinance its hefty debts. It is one of a growing number of victims of the government’s clean-up of the financial system, or what is known in China as the “regulatory storm”.

The storm has been gathering strength for the better part of a year but its intensity over the past couple of weeks has caught many off-guard. The government wasted little time after an important Communist party meeting in October before taking on some of the riskier parts of the financial system. As a result, China’s risk-free interest rate—ie, the yield on government bonds— has shot up. Overall, it has risen by a percentage point since the start of 2017.

For firms, even those closely tied to the state, the rise in borrowing costs has been even steeper. The yield on ten-year bonds issued by China Development Bank, a “policy bank” that finances state projects at home and abroad, has soared to nearly 5%, the highest in three years (see chart).

...

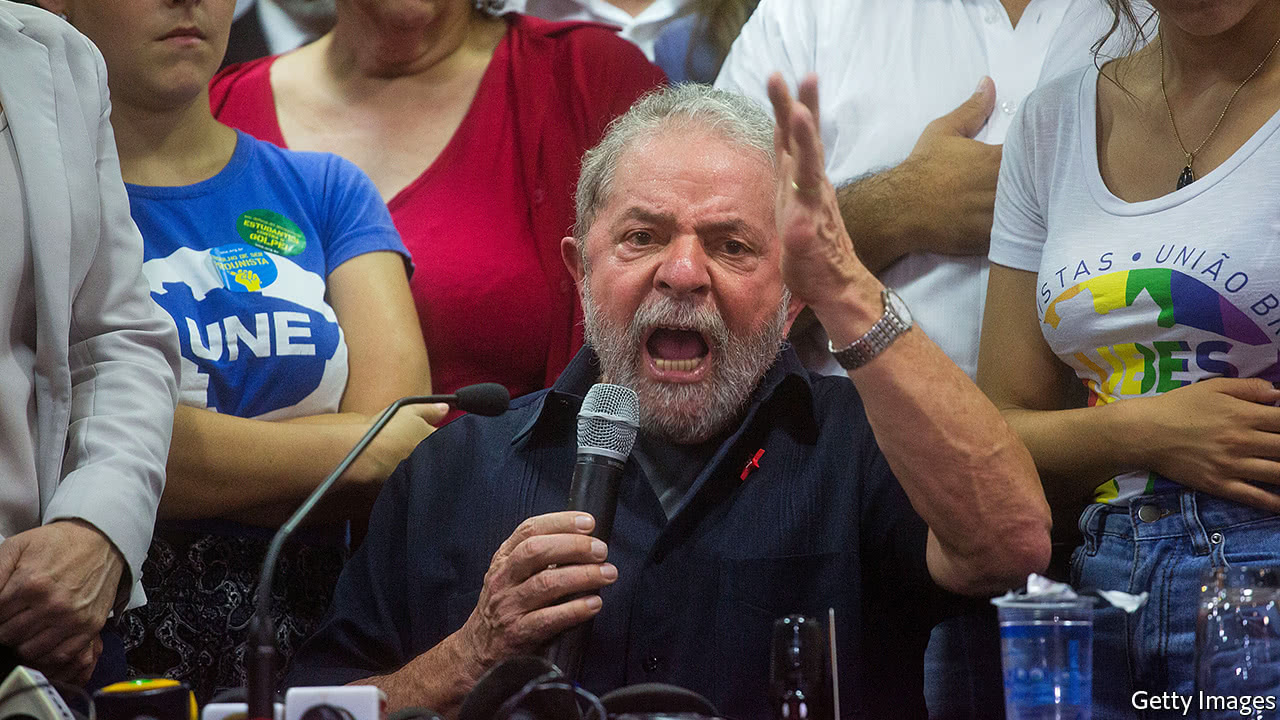

Brazil puts its state development bank on a diet

{kind=link}

IN 2009, as Brazil was buffeted by the global financial crisis, its president, Luiz Inácio Lula da Silva, was seething. The mess, he complained, was the fault of “blue-eyed white people, who previously seemed to know everything, and now demonstrate they know nothing at all”. For him the crisis was a repudiation of Anglo-Saxon liberalism and a vindication of state capitalism. Like many countries, Brazil cut interest rates and increased spending. Unlike many other governments, however, Brazil’s used its state development bank, BNDES, to funnel subsidised credit to Brazil’s largest companies. Thanks to cheap loans from the Treasury, the bank doubled its lending, which reached a peak of 4.3% of GDP in 2010. For most loans the interest rates were half the level of Selic, the central bank’s benchmark.

The plan worked, for a while. Brazil emerged from the crisis relatively unscathed: after a short recession in 2009 the economy rebounded...

India’s new bankruptcy code takes aim at delinquent tycoons

{kind=link}

A SMOOTH bankruptcy process is akin to reincarnation: a company at death’s door gets to shuffle off its old debts, often gain new owners, and start a new life. Might the idea catch on in India? A first wave of cadaverous firms are seeking rebirth under a bankruptcy code adopted in December 2016. In a hopeful development, tycoons once able to hold on to “their” businesses even as banks got stiffed seem likely to be forced to cede control.

India badly needs a fresh approach to insolvent businesses. Its banks’ balance-sheets sag under 8.4trn rupees ($130bn) of loans that will probably not be repaid—over 10% of their outstanding loans. But foreclosure is fiddly: it currently takes over four years to process an insolvency, and recovery rates are a lousy 26%. Partly as a result, bankers have often turned a blind eye to firms they ought to have foreclosed on.

This is bad for the banks and worse for the economy, which has slowed markedly, in part as credit to companies has dried up. The problem festered for years, not...

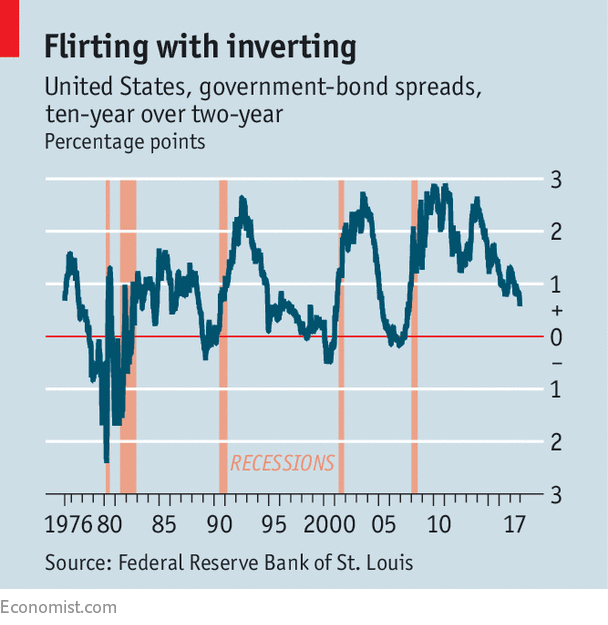

A flattening yield curve argues against higher interest rates

CENTRAL bankers may control short-term interest rates, but long-term ones are mostly free to wander. They do not always behave. When Alan Greenspan, then chairman of the Federal Reserve, was raising short rates in 2005, he described a simultaneous decline in long rates as a “conundrum”. His successor-to-be, Ben Bernanke, blamed foreign investments in American assets because of a “global saving glut”.

Janet Yellen, today’s (outgoing) Fed chair, faces a similar puzzle. Ms Yellen’s Fed has raised rates twice this year, and will probably make it three times in December. In October the Fed began to reverse quantitative easing (QE), purchases of financial assets with newly created money. Despite all this monetary tightening, yields on ten-year Treasury bonds have fallen from around 2.5% at the start of 2017 to about 2.3% today. As a result, the “yield curve” is flattening. The difference between ten-year and two-year interest rates is at its lowest since November 2007 (see chart).

{kind=link}

The...

What cheese can tell you about international barriers to trade

{kind=link}

BEN SKAILES, a British cheesemaker, is busy as Christmas ripens demand for his Stilton. Foreigners make up a third of demand for his dairy, Cropwell Bishop Creamery. This exporting achievement is not to be sniffed at when one considers the barriers to the cheese trade.

Some are natural. Perishable food goes better with wine than long journeys. At least Mr Skailes’s Stilton can survive the three-week trip to America. (His is best eaten within 16 weeks.) Softer cheeses struggle, giving American producers an advantage.

Other hurdles are man-made. Tariffs and quotas are supposed to support domestic dairy industries, and are more onerous than in other sectors. The European Union protects its dairy industry with a 34% average duty, compared with an overall average of 5%. In America it is 17%, compared with 3.5%. Stilton escapes American quotas, but full “loaves” are taxed at a 12.8% rate, or 17% if they arrive sliced. (Unprocessed...